Weekly Capital Flow Analysis

【Weekly Capital Market Tone (Macro Market Verdict)】

This week's capital market shows a divergence at high levels. Capital flowed out of overbought IC design stocks, refocusing on Tier 1 AI infrastructure cores—particularly strong momentum ASICs and bottoming-out ABF/CCL substrates. Meanwhile, Domestic Fund Managers performed offensive-defensive rotations in Tier 2, moving some capital into low-base safe havens while remaining locked into automation and niche equipment stocks. Tier 3 is dominated by Speculative Capital, strongly igniting semiconductor consumables and precision industries with high fundamental support, forming a new trend amidst sector rotation.

【EDGE Quantitative Model and Battlefield Rules Declaration (The EDGE Framework)】

Our core discipline is simple: don't guess the bottom, don't look for laggard catch-up plays, only capture the leaders with the strongest price momentum and most concentrated capital in the entire market. To achieve this, we divide the market into three independent capital battlefields:

- Liquidity Tiers (Tier 1~3):Tier 1 (Liquidity Top 1-50) is the macro battlefield dominated by Foreign Institutional Investors, determining the market direction; Tier 2 (Top 51-400) is the industrial battlefield for Domestic Fund Managers' positioning, focusing on medium-term trends; Tier 3 (Top 401-1000) is the niche theme battlefield where Speculative Capital and local investors compete, exhibiting the highest volatility.

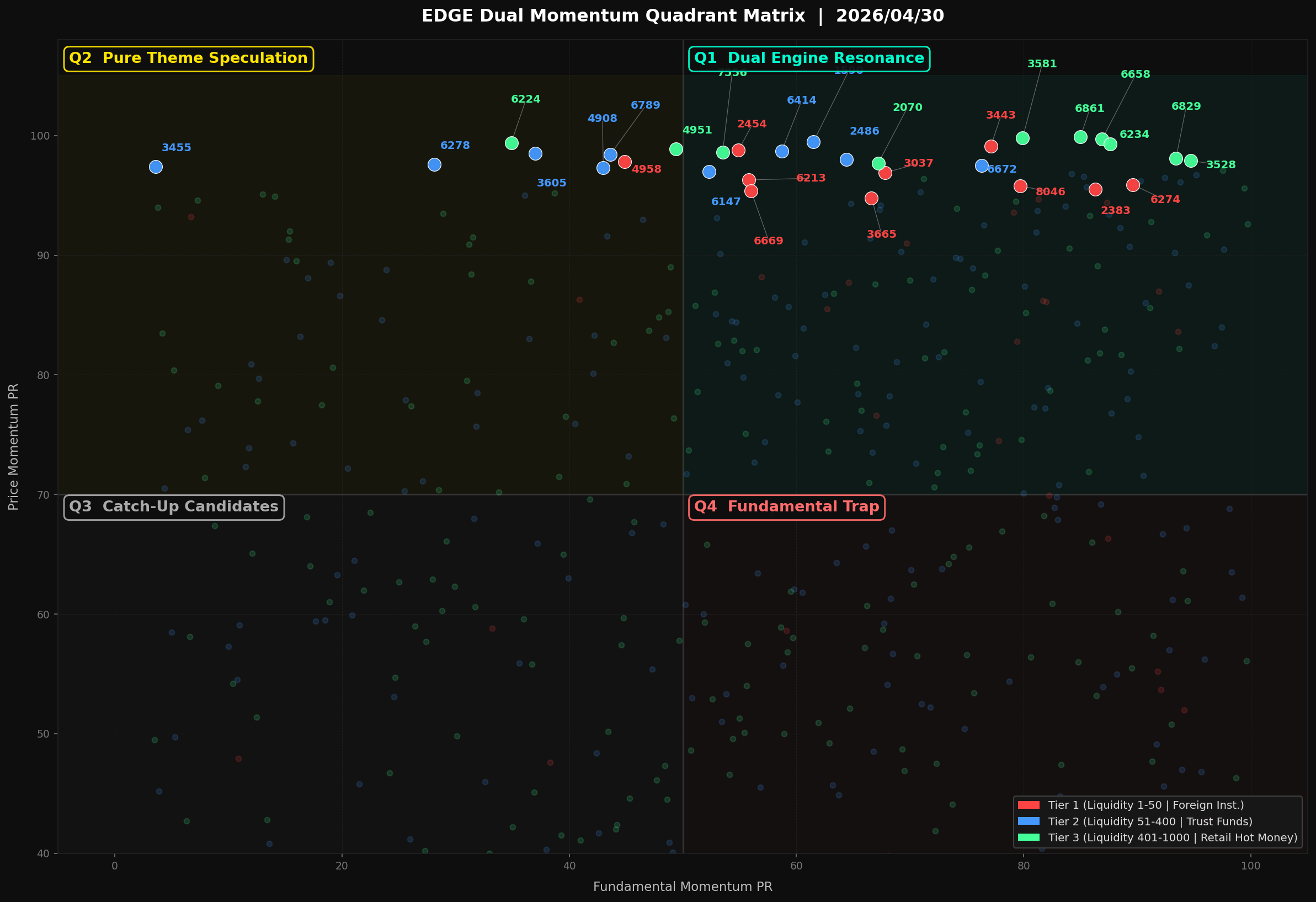

- Four-Quadrant Matrix:All targets are positioned via the X-axis "EDGE Fundamental PR Score" and Y-axis "EDGE Momentum PR Score." The upper-right quadrant is 【Dual-Engine Resonance】, representing targets with both strong fundamentals and capital momentum—our core prey; the upper-left quadrant is 【Momentum-Driven Rally】, representing weak fundamentals but strong capital momentum—high-risk pure speculative targets.

Market focus this week is extremely concentrated, centered around three main themes:

- AI Computing Power and High-Speed Substrate Supply Chain:Foreign Institutional Investors' macro battlefield, showing 【Dual-Engine Resonance】 in fundamentals and capital momentum.

- Smart Manufacturing and Advanced Packaging/Testing Equipment:Domestic Fund Managers' mid-cap battlefield; some stocks show 【Momentum-Driven Rally】, requiring strict control over fundamental decoupling risks.

- Semiconductor Consumables and Precision Industry:Niche battlefield ignited by Speculative Capital, mostly 【Dual-Engine Resonance】 hidden champions with high fundamental support.

Quantitative data for all focus themes and indicator stocks are marked in the 【Dual-Track Core Matrix】 below.

EDGE Dual-Track Core Matrix

Tier 1|Foreign Institutional Investors Macro Battlefield

- Battlefield Attribute:Tier 1(Liquidity Top 1-50)|Foreign Institutional Investors Macro Battlefield

- Main Theme of the Week:AI Computing Power and High-Speed Substrate Supply Chain. Foreign Institutional Investors are heavily betting on AI infrastructure, especially ASIC, CCL, and ABF substrates, with fundamentals and momentum strengthening simultaneously.

| EDGE Momentum PR Score | Stock Ticker and Name | Core Capital Theme |

|---|---|---|

| 99.1 | 3443 GUC | 【Dual-Engine Resonance】Strong ASIC demand, Foreign Institutional Investors raising target prices, extremely strong momentum. |

| 98.8 | 2454 MediaTek | Mobile AI chip market share increasing, optimistic outlook from investor conference. |

| 97.8 | 4958 Zhen Ding Tech | PCB industry recovery, Foreign Institutional Investors covering at lows driving a Momentum-Driven Rally. |

| 96.9 | 3037 Unimicron | ABF substrate utilization rates recovering, fundamentals bottoming out and rebounding. |

| 96.3 | 6213 EMC | Server board upgrades driving revenue momentum and capital pursuit. |

| 95.9 | 6274 Iteq | High-frequency/high-speed board demand is strong, excellent fundamental data. |

| 95.8 | 8046 Nan Ya PCB | Substrate industry inventory depletion finished, significant Foreign Institutional Investor entry. |

| 95.5 | 2383 TUC | 【Dual-Engine Resonance】Leader in AI server CCL, profitability significantly improved. |

| 95.4 | 6669 Wiwynn | Cloud Service Providers (CSP) capital expenditure increasing, revenue remains at high levels. |

| 94.8 | 3665 Bizlink | Explosive demand for automotive and AI transmission cables, robust profit structure. |

Tier 2|Domestic Fund Managers Mid-Cap Growth Stocks

- Battlefield Attribute:Tier 2(Liquidity Top 51-400)|Domestic Fund Managers Mid-Cap Growth Stocks

- Main Theme of the Week:Smart Manufacturing and Advanced Packaging/Testing Equipment. Domestic Fund Managers focus on automation and semiconductor equipment; fundamentals of some stocks have not yet caught up, beware of risks when chasing highs.

| EDGE Momentum PR Score | Stock Ticker and Name | Core Capital Theme |

|---|---|---|

| 99.5 | 1590 Airtac | 【Dual-Engine Resonance】Automation demand recovery, active positioning by Domestic Fund Managers driving momentum. |

| 98.7 | 6414 S&T | Industrial PC transitioning to AI, revenue structure optimization attracting buyers. |

| 98.5 | 3605 ACES | Connector spec upgrades, high short-term willingness from Domestic Fund Managers to chase prices. |

| 98.4 | 6789 VisEra | CIS packaging/testing demand strengthening, capital flowing into the semiconductor sector. |

| 98.0 | 2486 I-Chiun | Heat spreaders entering AI chain, both momentum and fundamentals are excellent. |

| 97.6 | 6278 TSE | Mini LED penetration increasing, low base driving a Momentum-Driven Rally. |

| 97.5 | 6672 Elite Material | 【Dual-Engine Resonance】Stable automotive CCL shipments, strong fundamental support. |

| 97.4 | 3455 UTC | AOI equipment theme is hot, but fundamental data is extremely low, warranting caution. |

| 97.3 | 4908 PRiVO | Strong demand for optical communication modules, Domestic Fund Managers locking in positions driving a Momentum-Driven Rally. |

| 97.0 | 6147 ChipMOS | Display driver IC packaging/testing recovering, a top choice for a capital safe haven. |

Tier 3|Speculative Capital Dominated Speculative Play

- Battlefield Attribute:Tier 3(Liquidity Top 401-1000)|Speculative Capital Dominated Speculative Play

- Main Theme of the Week:Semiconductor Consumables and Precision Industry. Small-cap niche stocks show extremely strong momentum, most with very high EDGE Fundamental PR Scores, suitable for finding catch-up opportunities.

| EDGE Momentum PR Score | Stock Ticker and Name | Core Capital Theme |

|---|---|---|

| 99.9 | 6861 Iray | Breakthrough in medical AI imaging technology, Speculative Capital strongly pushing momentum. |

| 99.8 | 3581 Epoch | Strong demand for semiconductor test consumables, excellent fundamental performance. |

| 99.7 | 6658 PSI | Leader in PCB automation equipment, dual growth in profits and momentum. |

| 99.4 | 6224 Polytronics | Overcurrent protection components recovering, active short-term capital pursuit. |

| 99.3 | 6234 Goan-Air | High visibility for precision equipment orders, strong fundamental support. |

| 98.9 | 4951 Princeton | Laptop IC inventory restocking, Speculative Capital short-term Momentum-Driven Rally. |

| 98.6 | 7556 IDS | Localization of semiconductor consumables, strong continuous profit growth momentum. |

| 98.1 | 6829 Chien Fu Precision | 【Dual-Engine Resonance】Dual themes of defense and semiconductors, extremely high EDGE Fundamental PR Score. |

| 97.9 | 3528 Answer Tech | 【Dual-Engine Resonance】Diverse product distribution lines, fundamental data is the highest in the sector. |

| 97.7 | 2070 Sun-Same | Strong exports of screw inspection equipment, profit momentum remains high. |

Thematic Macro-Logic | AI Computing Power and High-Speed Substrate Supply Chain

【Thematic Macro-Logic】

AI computing power competition has evolved from individual GPU procurement into a comprehensive arms race by Cloud Service Providers (CSPs) seeking optimization of power consumption and cost. At the core of this structural shift is the dual-track advancement of general-purpose GPUs and customized ASIC chips, leading to a non-linear upgrade of the underlying specifications of computing infrastructure. The NRE-to-ASIC business model is creating a new, long-cycle growth curve for IC design services and Silicon IP providers, and this is only the first ripple. High computing power inevitably accompanies high-bandwidth data transmission needs. From intra-chip and inter-package to server node interconnection, transmission speeds are driving toward PCIe 5.0/6.0 and CXL generations, challenging the physical limits of signal-carrying materials and substrates.

The reason this track receives a valuation premium from "smart money" in the Tier 1 macro battlefield lies in the multiplier effect of its "Dual-Engine Resonance" and high financial predictability. The market no longer views these as traditional cyclical electronics stocks but defines them as "spec-setters" and "core enablers" of AI infrastructure. Capital is willing to pay a high premium now, betting on the explosion of royalties and mass production revenue triggered by AI ASIC tape-outs transitioning to volume production over the next 2-4 quarters, as well as product mix optimization and structural gross margin improvements brought by the accelerated adoption of high-end CCL (Copper Clad Laminate) in new server platforms. This is a re-rating based on the increase in "content value" rather than a simple expectation of volume growth.

Core Leaders Micro-Insights

【Core Leaders Micro-Insights】

🎯 Core Leader Insight: 3443 GUC

(1) Absolute Moat and Supply Chain Positioning

The absolute moat of 3443 GUC stems from its strategic positioning as a "value chain extension" of TSMC. As the most critical ASIC design service partner in the TSMC ecosystem, GUC not only holds priority access to the most advanced processes (3nm/2nm) and advanced packaging (CoWoS/SoIC) but is also deeply involved in the entire process from specification definition to chip realization for top-tier North American CSP customers. In the AI ASIC field, this means GUC is not just a design service provider but a hub connecting cloud giants, IP providers, and the world's top wafer foundries. Its position is not merely technical leadership but a structural advantage based on trust, long-term cooperation, and process integration capabilities, making it an unavoidable key node for CSP giants realizing their AI strategic blueprints.

(2) Momentum Catalysts (Recent Marginal Changes)

The core catalyst for market momentum comes from the AI ASIC projects of large North American CSP customers accelerating from the high-margin NRE (Non-Recurring Engineering) phase into the larger-scale Turnkey (mass production) phase. The significance of this marginal change is that the revenue structure will shift from one-time project income to long-term, high-visibility mass production contributions. EDGE Momentum PR Score as high as 99.1 reflects that the market has viewed the successful mass production of several large-scale AI/HPC projects as high-probability events and has priced-in the massive revenue and profit contributions for the coming years. Every piece of information regarding customer tape-out progress or CoWoS capacity allocation will reinforce this expectation, serving as direct fuel for the stock price.

(3) Dual-Track Fundamental Verification

Applying the "Dual-Engine Resonance" strategic label, 3443 GUC is the primary engine driving "AI Computing Power." Its fundamental verification path is clear: First, observe the sustained growth and high-level maintenance of NRE revenue, which represents the rising quality and quantity of projects on hand and serves as a leading indicator for future mass production business. Second, verify the structural increase in Turnkey revenue share and the accompanying stable or slightly rising gross margins, which will prove the scalability and profitability of its business model. EDGE Fundamental PR Score 77.1 while not at the very top, reflects its superior growth prospects and profit structure compared to traditional IC design companies. The market expects a significant step-up in operating cash flow and ROE once mass production scales up.

🎯 Core Leader Insight: 2383 TUC

(1) Absolute Moat and Supply Chain Positioning

The moat of 2383 TUC is built on a deep accumulation of material science, especially in the field of high-speed, low-loss (Low Loss) CCL required for AI servers, where it has formed a practical oligopoly. As transmission rates move from 112G to 224G, signal attenuation and distortion issues amplify exponentially, placing extremely strict requirements on the Dk/Df (dielectric constant/dielectric loss) values of CCL. TUC, with its leading halogen-free environmentally friendly material technology and market share advantage in M6/M7 grade (Very Low Loss/Ultra Low Loss) materials, is deeply integrated into the global supply chain for mainstream AI GPU/ASIC accelerator cards, high-speed switches, and server motherboards. It is not just a material supplier but one of the "material standard definers" for the next generation of high-performance computing platforms, with extremely high customer switching costs.

(2) Momentum Catalysts (Recent Marginal Changes)

Marginal catalysts for momentum come from the "acceleration" and "popularization" of AI server platform upgrades. Next-generation platforms from NVIDIA, AMD, and Intel not only mandate the use of Ultra Low Loss materials on the main processor OAM (OCP Accelerator Module) substrate but also simultaneously upgrade material specs for peripheral CPU motherboards, switch boards, and Retimer/Redriver boards. This trend leads to a double pull in TUC's high-end material penetration and content per box within a single server. EDGE Momentum PR Score 95.5 reflects strong market expectations for this spec upgrade cycle. Any news regarding upward revisions in AI server shipments or early adoption of new platforms will translate directly into positive expectations for its revenue and profit.

(3) Dual-Track Fundamental Verification

Under this "Dual-Engine Resonance" framework, 2383 TUC is the second engine for "High-Speed Materials and Substrate Upgrades," directly capturing the overflow benefits of the computing power explosion. Its fundamental verification path lies in the "structural optimization" of financial report quality: First, observe whether the revenue share of high-end materials applied to AI servers and 800G switches continues to climb. Second, monitor changes in gross margin and operating margin, which are the most direct financial reflections of an increased proportion of high-end product shipments. EDGE Fundamental PR Score as high as 86.3 confirms its excellent profitability and operational efficiency. The market expects that as the proportion of AI-related applications breaks through key thresholds, TUC's profit levels will decouple from the consumer electronics business cycle, showing an independent and steeper growth curve.

Thematic Macro-Logic | Smart Manufacturing and Advanced Packaging/Testing Equipment

【Thematic Macro-Logic】

In the post-globalization era, supply chain resilience has replaced cost-efficiency as the core consideration for corporate layout. This structural transformation is injecting a long-term and strong tailwind into the fields of smart manufacturing and advanced packaging and testing equipment. Geopolitical risks are prompting strategic industries such as semiconductors and AI servers to accelerate regionalization of production capacity, thereby triggering massive capital expenditure demand for automated production lines and precision manufacturing equipment. The evolution of technical specifications is an even more critical driver. The reliance of AI and HPC chips on 2.5D/3D packaging technologies like CoWoS directly increases the demand for high-precision, high-stability packaging and testing equipment, with a clear supply-demand gap.

Tier 2 Domestic Fund Managers entering at this stage follow a trading logic that is not simply chasing cyclical recovery but a re-rating of the long-term narrative of "localization replacement." The equipment market, previously monopolized by Japanese, German, and American giants, is opening a strategic gap due to supply chain security concerns, giving high-tech local manufacturers an excellent opportunity to enter the high-end market. Smart money is willing to grant a higher valuation premium now, expecting a "Davis Double" of market share and gross margin for these companies. The market is pricing-in excess revenue growth and profit structure improvements over the next 2-4 quarters due to order diversion effects and product mix optimization, rather than just a linear extrapolation of past financial reports.

Core Leaders Micro-Insights

【Core Leaders Micro-Insights】

🎯 Core Leaders Insights: 1590 Airtac

(1) Absolute Moat and Supply Chain Position

Airtac is already a giant that cannot be ignored in the global pneumatic component market. Its moat is built on extensive distribution channels in the China market, a highly competitive cost structure, and the flexibility to respond quickly to customer needs. As the "joints" and "muscles" of automation equipment, pneumatic components are fundamental components for all smart manufacturing scenarios, indispensable from traditional production lines to high-end electronic assembly. Its status is equivalent to an "arms dealer" in the field of automation, directly benefiting from the expansion of capital expenditures in the overall manufacturing industry.

(2) Momentum Catalysts (Recent Marginal Changes)

Marginal momentum comes from the structural shift in its product applications. Airtac is aggressively moving from traditional general-purpose industrial applications into high-growth, high-margin industries such as photovoltaics, lithium batteries, semiconductors, and electronic assembly. This optimization of the product portfolio not only increases the Average Selling Price (ASP) but, more crucially, creates a stronger linkage between its operational performance and the business cycles of specific high-growth sectors, breaking away from the previous single-linkage with China's overall manufacturing PMI.

(3) Dual-Track Fundamental Validation

This target perfectly illustrates the psychological expectations of a 【Momentum-Driven Rally】. Its EDGE Momentum PR Score (99.5) is much higher than its EDGE Fundamental PR Score (61.5), reflecting that the market is trading on the "future" rather than the "past." Domestic Fund Managers are targeting the potential for Airtac to gradually replace Japanese competitors such as SMC in the high-end electronics industry under the logic of "localization replacement." Institutional investors expect this replacement trend to be validated in future financial reports through the continuous climb of gross margins and an increase in the revenue share of high-end product lines; the current high momentum is an early reaction to this expectation.

🎯 Core Leaders Insights: 6672 Elite Material

(1) Absolute Moat and Supply Chain Position

Elite Material's moat lies in its technical depth in niche markets. The company focuses on high-frequency, high-speed, and high-heat dissipation copper clad laminates (CCL) required for military, aerospace, network communications, and semiconductor testing interfaces. Compared to commodity CCL used in consumer electronics, its products have extremely high certification thresholds and customer stickiness. In the advanced packaging and testing supply chain, Elite Material plays the role of a key material supplier, and its material performance directly determines the yield and stability of testing interfaces such as Probe Cards and Load Boards.

(2) Momentum Catalysts (Recent Marginal Changes)

The squeeze on advanced packaging and testing capacity by AI chips is its strongest momentum catalyst. From CoWoS to HBM, complex chip structures have significantly increased testing complexity and time, leading to exponential growth in requirements for durability and signal integrity of testing interface materials. Elite Material's special materials suitable for high-end testing are at the core of this round of the AI hardware arms race, with extremely high demand visibility, becoming one of the links with the highest technical value in the semiconductor equipment localization chain.

(3) Dual-Track Fundamental Validation

Unlike Airtac, Elite Material's EDGE Momentum PR Score (97.5) and EDGE Fundamental PR Score (76.3) show a dual-high pattern, indicating that its growth story has begun to materialize in financial reports. The logic of Domestic Fund Managers locking in positions is based on the trend of 【Localization Replacement】, where it has successfully secured a spot in the supply chains of major global testing interface manufacturers, and this trend is accelerating. Institutional investors are validating its market share gains in the AI testing materials field through its quarter-on-quarter revenue and gross margin performance. Concurrent high momentum and high fundamentals indicate that it is currently in the main upward phase of the industry upcycle and market share expansion.

Thematic Macro-Logic | Semiconductor Consumables and Precision Industry

Capital flows in the semiconductor industry are entering a more refined stratification phase. While the market spotlight and large-scale capital remain concentrated in Tier 1 core battlefields such as foundry leaders and AI chip design giants, Tier 3 Speculative Capital seeking alpha has quietly shifted toward niche areas within the supply chain where operating leverage is about to be released. Semiconductor consumables and precision industries are perfect hunting grounds for such smart money. The underlying drivers come from three structural shifts: 1. The complexity of advanced processes (e.g., 3nm/2nm) and advanced packaging (CoWoS) is growing exponentially, significantly increasing the consumption rate and specification requirements for high-purity, high-precision consumables and key components; 2. Global supply chain restructuring driven by geopolitics has provided unprecedented opportunities for localization replacement and order shifts for local suppliers with certification and mass production capabilities; 3. Terminal demand is recovering from the bottom, and fab capacity utilization is rebounding, directly catalyzing the pull-in momentum for maintenance, replacement parts, and regular consumables.

At this point in time, Speculative Capital is willing to give these "hidden champions" a higher valuation premium. The core logic of the trade is not based on realized historical financials, but on the expected discounting of "high-certainty earnings revisions" within the next 2-3 quarters. The market expects that as fab customers' utilization rates climb and new plant capacity comes online, order visibility for these companies will significantly lengthen, accompanied by an increase in the proportion of high-margin product portfolios, thereby driving double-digit growth in revenue and gross margins. This smart money is betting that current market consensus has not yet fully reflected their upside earnings potential. Once financial figures begin to materialize quarter by quarter, it will trigger a broader re-rating rally. The safety margin provided by high fundamentals serves as a solid backstop for Speculative Capital engaged in high-risk momentum trading.

Core Leaders Micro-Insights

🎯 Core Leader Insight: 3528 Answer Tech

(1) Absolute Moat and Supply Chain Position

3528 Answer Tech, as a niche semiconductor distributor, possesses a moat that is not derived from manufacturing but is built upon irreplaceable "technical integration" and "key product line representation." The company has long cultivated high-entry-barrier applications such as industrial automation, defense, and high-end computing, holding key agency lines for AMD-Xilinx FPGAs and ADI's high-end analog components. Its core value lies not just in selling components but in acting as a solution provider that offers deep collaborative design and technical support. This high-stickiness service model constructs strong customer barriers, allowing it to play an indispensable role as an enabler within the supply chain.

(2) Momentum Catalyst (Recent Marginal Changes)

The trigger for momentum lies in the trend of AI applications spreading from the cloud to the edge (Edge AI). The AMD-Xilinx FPGA chips it represents are seeing rapidly rising demand in industrial robotics, smart factories, and AI visual inspection due to their low-latency and programmable characteristics. The marginal change is that while industrial PCs were the primary driver in the past, strong pull-in momentum from AI-related applications has now been added. The market is re-evaluating the value of Answer Tech as a "hidden AI concept stock," and this valuation gap has become the core catalyst attracting the influx of Speculative Capital recently.

(3) Dual-Track Fundamental Verification

This is a classic case of 【Dual-Engine Resonance】. Its EDGE Fundamental PR Score of 94.7 is reflected in the company's past stable profitability, healthy cash flow, and high dividend policy, which serve as the "fundamental anchor" supporting the stock price. The recent intervention of Speculative Capital acts as the "momentum wing" for its new growth curve. The verification of financial report quality will manifest in two ways: first, whether the proportion of high-margin product lines like AMD-Xilinx continues to rise within the revenue structure; and second, observing whether inventory turnover days remain at a healthy level alongside revenue growth. This will confirm the authenticity of demand growth rather than simple inventory accumulation.

🎯 Core Leader Insight: 6829 Chien Fu Precision

(1) Absolute Moat and Supply Chain Position

The moat of 6829 Chien Fu Precision is built upon ultimate "precision machining processes" and "top-tier customer certifications." As a core supplier to the global semiconductor equipment leader Applied Materials, the company specializes in providing high-cleanliness, high-precision vacuum chambers and key components. Entering the semiconductor front-end equipment supply chain requires a long and rigorous certification cycle; once successfully positioned, the company enjoys extremely high customer stickiness and order stability. Its position in the supply chain is equivalent to being a key ordnance manufacturer in the semiconductor equipment "arsenal," where technology and quality are its deepest barriers.

(2) Momentum Catalyst (Recent Marginal Changes)

The momentum catalyst stems from the restart of a new round of global wafer fab capital expenditure cycles. As major manufacturers like TSMC and Intel expand aggressively in the US, Japan, and other regions, demand for semiconductor equipment is seeing structural growth. The most significant marginal change is that order visibility has extended from a few months in the past to over a year. The market expects Chien Fu Precision to benefit not only from the pull-in of new equipment but also from the massive aftermarket (AM) repair and replacement market following the installation of new plants in the coming years—a long-term cash flow business with even higher margins.

(3) Dual-Track Fundamental Verification

This ticker represents the combination of "certainty" and "explosiveness." An EDGE Fundamental PR Score of 93.4 comes from its long-term partnerships with first-tier manufacturers, stable orders, and excellent yield control capabilities. What Speculative Capital is trading on is the "explosiveness" of its impending operating leverage release. The focus of financial report quality verification will fall on: first, the ramp-up speed of capacity utilization, which will directly determine the expansion of gross and operating margins; and second, changes in the backlog amount, which will be the most direct indicator for predicting revenue momentum over the next 6-12 months. Once financial reports show revenue growth outstripping expense growth and a significant upward inflection point in profitability, the current momentum trend will be validated.

This week, the TAIEX exhibited high-level volatility amid massive turnover, with the electronics sector carrying the load, its share of turnover once exceeding 70%, reflecting highly concentrated capital. The protagonists are undoubtedly the AI computing and high-speed substrate supply chains; benchmark stocks, driven by positive revenue news, hit new periodic highs on heavy volume, becoming the sole consensus for market chasing. In contrast, smart manufacturing and advanced packaging equipment groups showed divergence; some stocks locked by Domestic Fund Managers continued to edge higher along moving averages, but some overextended stocks showed signs of price-volume divergence, indicating that "chips" (shareholder stability) are starting to loosen. Semiconductor consumables and precision industry acted as steadying forces; though not the market focus, their solid fundamentals attracted defensive capital inflows during market fluctuations. Regarding marginal changes, we observed some capital spilling over from overextended Tier 1 AI core stocks to lower-positioned Tier 2 electronics, such as CCL, high-end PCB, and certain LED groups, suggesting the market is preparing for potential sector rotation.

The AI computing and high-speed substrate supply chains are currently in the accelerated peak phase of the primary upward wave. Leaders such as AI ASIC and ABF substrate plants saw price and volume rise in tandem this week. While the K-lines closed with long reds, the trading volume expanded to historical highs, implying intensifying signals of bullish-bearish divergence. Although the strong fundamentals of AI server demand are unquestionable, overheated indicators and deviation rates suggest that next week's market will transition from a one-sided rally to high-level violent volatility. If this trend continues, capital will further broaden its reach, moving from core chips and substrates to seek peripheral supply chains that haven't fully reacted, such as thermal modules, high-frequency connectors, cases, and power management units (PMUs), forming a compensatory rally pattern.

The momentum of smart manufacturing and advanced packaging equipment has transitioned from a general surge into a rotation of individual stock performances. The core driver of this theme comes from the continuous positioning of Domestic Fund Managers; therefore, the key observation point is the stability of holdings. Some leading stocks showed long upper shadows at high levels, suggesting the coexistence of break-even and profit-taking selling pressure, with signs of weakening momentum. However, as long as the outlook for semiconductor capital expenditure remains unchanged and the narrative of domestic substitution continues, capital will not fully withdraw. Instead, it will look within this group for stocks with lower price positions and more attractive valuations for switching. If first-tier equipment stocks turn to sideways consolidation next week, capital may flow toward second-tier testing and automation equipment plants where revenue turning points have just emerged.

Semiconductor consumables and precision industry are in a steady phase of rotating upward, exhibiting defensive-offensive characteristics backed by high fundamental support. Leading indicators for this group have not shown runaway surges but rather a solid step-like ascent, with a relatively healthy price-volume structure. In an atmosphere of market euphoria and the pursuit of high volatility, these "hidden champions" might not be the most dazzling stars, but their operational certainty and visibility make them excellent safe havens during capital rotation. If the broader market becomes more volatile, it is expected that more capital will move from high-positioned AI concept stocks into this area for safety, driving upward price comparisons for second-tier plants within the group that possess unique niches and excellent financial performance.

A market top is not determined by the strongest stocks, but by when capital can no longer find the next rotation target.

![[Semiconductor Consensus Tracking] 20260426 Trap Signals in the AI Frenzy](https://storage.ghost.io/c/45/e8/45e8af65-5e37-4e0a-95c0-7bd52e1935a5/content/images/size/w1200/2026/04/quadrant_20260426_en.png&q=100)