4-1-6 The Vanguard of the Pegatron Group — Kinsus (3189)'s Differentiated Survival and Resurgence

Kinsus (3189) initially dominated BT substrates and had a contact lens cash cow. Now, flush with cash, it enters AI; ABF capacity hits 85% off-season. Amid material gaps, Kinsus began 3-5% quarterly price hikes, approved Fab 6 high-end expansion, targeting GPU/ASIC/high-end networking, using a du...

To survive in the semiconductor component market, surrounded by formidable competitors, without an absolute advantage in scale, one must possess extremely shrewd 'battle-avoidance wisdom.' Kinsus, backed by the vast resources of the ASUS and Pegatron groups, very shrewdly avoided the brutal competition in the ABF substrate market, tightly controlled by Intel and Japanese manufacturers, in its early stages of development.

They concentrated their efforts on another equally massive battlefield, but one that required different material characteristics: BT substrates.

📱 Chapter 1: Avoiding the Red Ocean — The King of Memory and Mobile Phone BT Substrates

If you recall the material differences we discussed in [4-1-1]: ABF film is suitable for large-area, extremely fine-line PC and server chips (e.g., CPU/GPU); while another material called BT resin (Bismaleimide Triazine), although its circuitry cannot be as fine as ABF, possesses excellent dimensional stability and moisture resistance, making it highly suitable for consumer electronic products that are 'small in size, frequently dropped, or used in complex environments.'

Kinsus chose BT substrates as its fundamental foundation for survival and growth:

Cornerstone of Mobile and Communications: Kinsus secured substrate orders for baseband chips, radio frequency (RF) modules, and connectivity chips inside a massive number of smartphones globally.

Absolute Reliance in Memory: Whether it's DRAM in mobile phones or NAND Flash controllers in solid-state drives (SSDs), almost all of them rely on BT substrates.

By focusing on this niche market, Kinsus not only avoided direct confrontation with the two Japanese giants but also built a formidable moat of extremely high yield rates and scale in the BT substrate sector. Even today, BT substrates steadily contribute over one-third of Kinsus's substantial revenue.

👁️ Chapter 2: The Unconventional Masterstroke — The 'Contact Lens' Cash Cow That Weathered the Winter

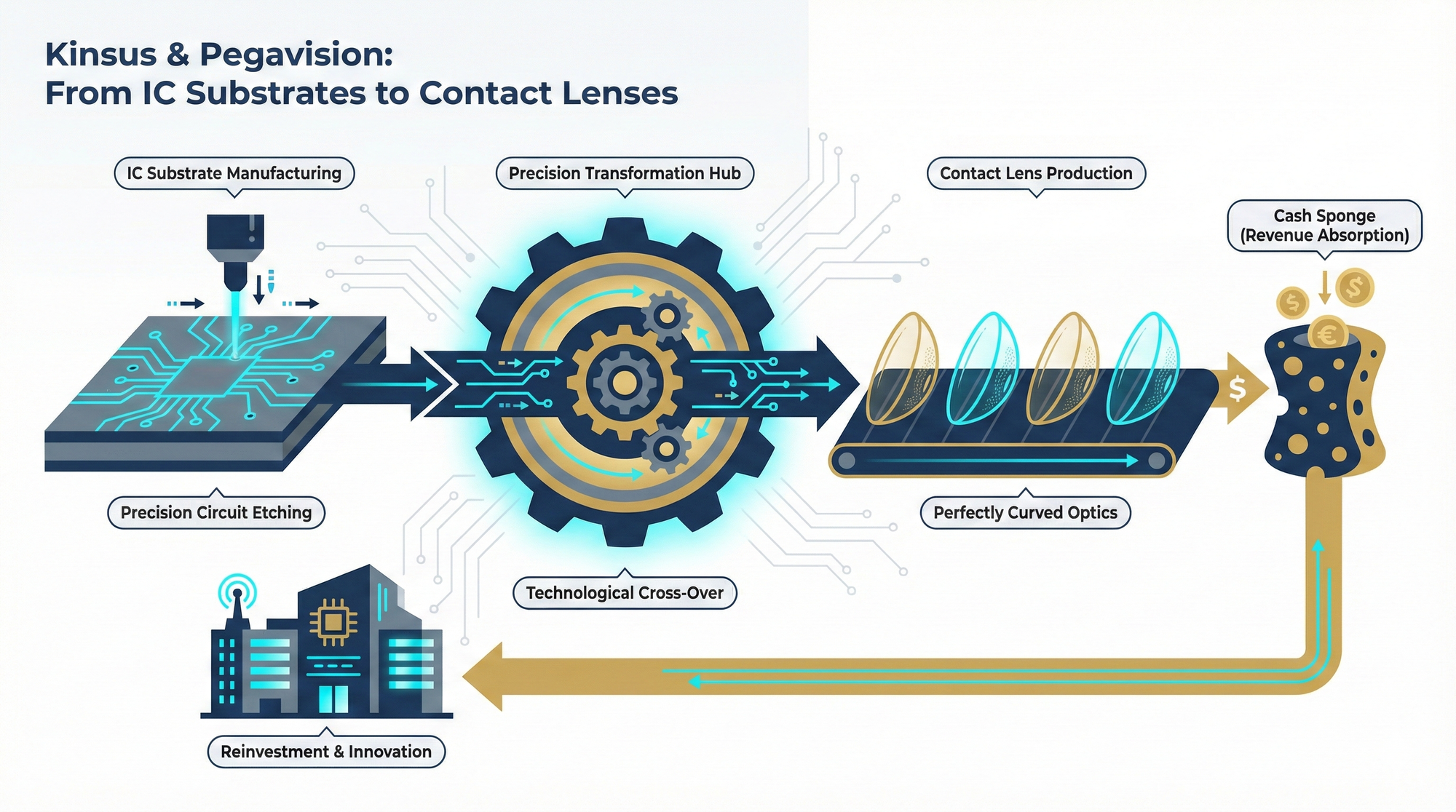

What truly astonished the capital market about Kinsus was its ultimate line of defense, one that no other semiconductor manufacturer possessed: a subsidiary that manufactures contact lenses.

You might find it absurd: how could a factory producing high-tech micron-level IC substrates also venture into disposable contact lenses? However, if you look at it from a 'process' perspective, it's actually a form of 'dimensional reduction attack' (i.e., applying advanced skills to a less complex field). Contact lens manufacturing also requires extremely precise 'mold development, optical design, and polymer chemical material formulation.' This bears a striking resemblance to the photolithography and lamination processes in the front-end of substrate manufacturing.

The Birth of Pegavision: Kinsus replicated its precise manufacturing management capabilities to contact lenses, giving birth to its subsidiary 'Pegavision'.

Resilient Cash Flow Sponge: The semiconductor industry is a brutal one, characterized by strong economic cycles (minor downturns every three years, major ones every five). When demand for consumer electronics weakens and idle substrate machinery causes competitors to incur substantial losses, Kinsus, however, relied on this 'consumer medical consumable' business, which is completely unaffected by the tech cycle and accounts for nearly 20% of its revenue, to generate a continuous stream of cash flow.

This cash cow allowed Kinsus, even during semiconductor downturns, to always have the confidence to persevere and even had the leeway to conduct R&D for next-generation technologies.

⚔️ Chapter 3: The Awakening in the AI Era — Entering the ABF Battlefield with Pockets Full of Cash

As time moved past 2024, the AI computing power arms race completely transformed industry rules. Kinsus's senior management clearly understood that while BT substrates could provide stable cash flow, with the smartphone and memory markets nearing saturation, BT substrates had lost their momentum for explosive growth.

The true vast ocean of opportunity lay in the ABF battlefield, which carried giant NVIDIA and ASIC chips.

With the substantial cash earned from BT substrates and contact lenses, coupled with the powerful system assembly and export support from the Pegatron Group, Kinsus decided to no longer remain on the sidelines. They officially reallocated their massive capital expenditures, making a significant move into the high-end ABF substrate sector, which they had previously avoided. They are now engaging in a final battle at the same table with Unimicron, Nanya PCB, and the two Japanese giants.

🚀 Chapter 4: Full Capacity Utilization Undeterred by Off-Season — The Strong Comeback of ABF Capacity

In the traditional consumer electronics cycle, the first quarter is typically the coldest off-season for the tech industry (revenue often faces double-digit sequential declines). However, for Kinsus today, the hunger for AI computing power has completely broken the physical laws of seasonality.

High Utilization Rate (UTR): The latest production line tracking data indicates that Kinsus's high-end ABF substrate capacity utilization rate surged to 85% in Q4 2025. Even more remarkably, this high 85% full capacity level remains unshaken as it enters Q1 2026, the traditional off-season.

Strong Fulfillment of Deferred Orders: Due to extremely strong demand for high-end HPC (High-Performance Computing), some orders that could not be processed in H2 2025 were directly deferred to Q1 2026. These high-margin AI orders perfectly filled the gap during the consumer electronics off-season, preventing Kinsus's production lines from even shutting down during the Lunar New Year.

📈 Chapter 5: T-Glass Shortages and the Profit Engine of 'Quarterly Price Hikes'

As we mentioned in the previous [Unimicron article], the severe shortage of T-Glass (low thermal expansion coefficient glass fiber cloth) is currently a critical bottleneck for high-end substrates. This macroeconomic constraint also affects Kinsus but concurrently grants the company extremely lucrative pricing power.

This post is for subscribers only

Sign up now to read the post and get access to the full library of posts for subscribers only.