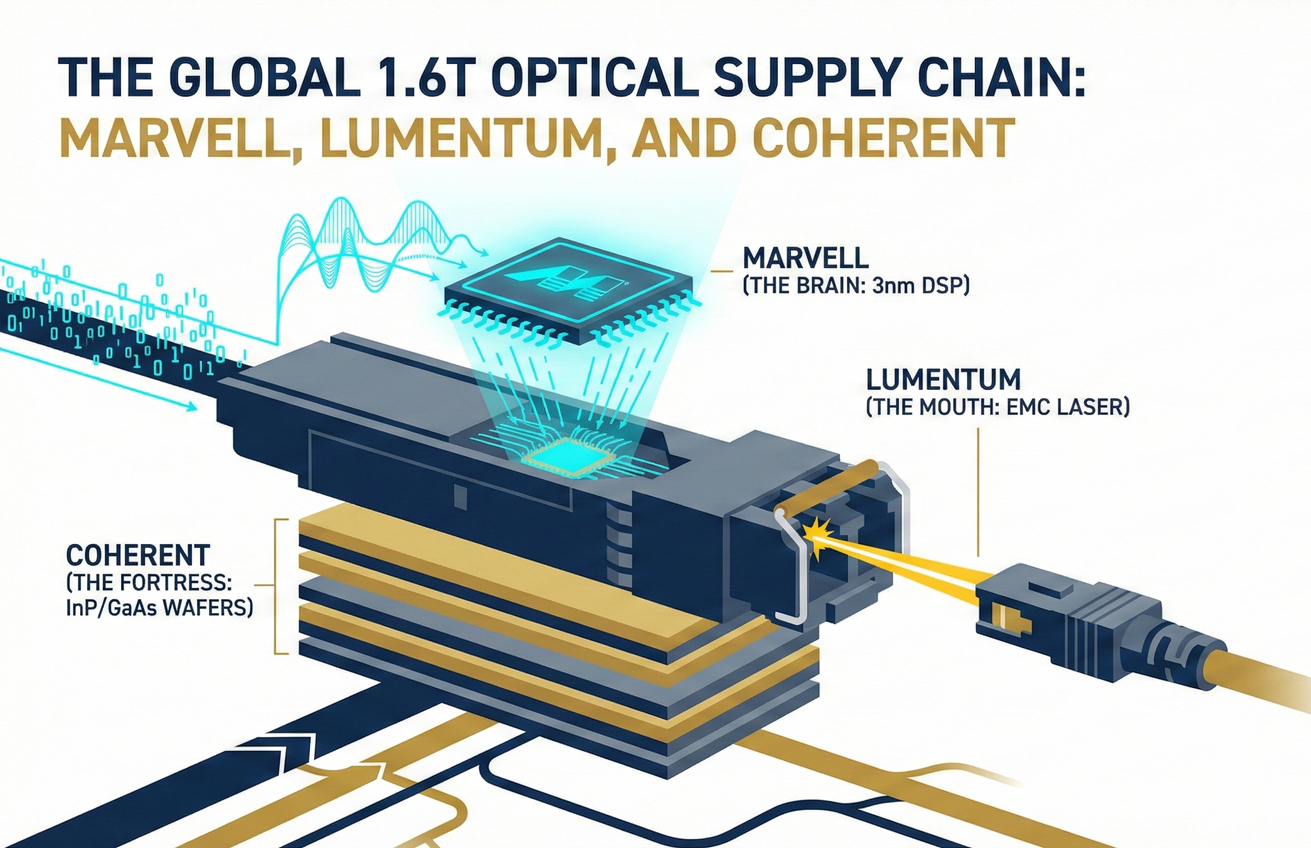

4-3-2 Global Optical Module Dominant Players: Marvell, Lumentum, and Coherent's 1.6T Monopoly Battle

The global 1.6T market is defined by three giants: Marvell levies a "brain tax" with its 3nm DSP chips; Lumentum defines mass production pace with EML laser chip capacity (40% expansion); and Coherent, leveraging vertically integrated indium phosphide materials and modules, secured historic major...

If PCBs are the skeleton of AI servers, then optical transceiver modules are the "mouth" and "ears" of this colossal beast. As we head towards 1.6T (1600G) in 2026 in this intergenerational arms race, this is no longer just a simple hardware upgrade, but an ultimate battle against physical signal attenuation.

🧠 Chapter One: The Brain of the Signal — Marvell (MRVL) and the 1.6T Bottleneck

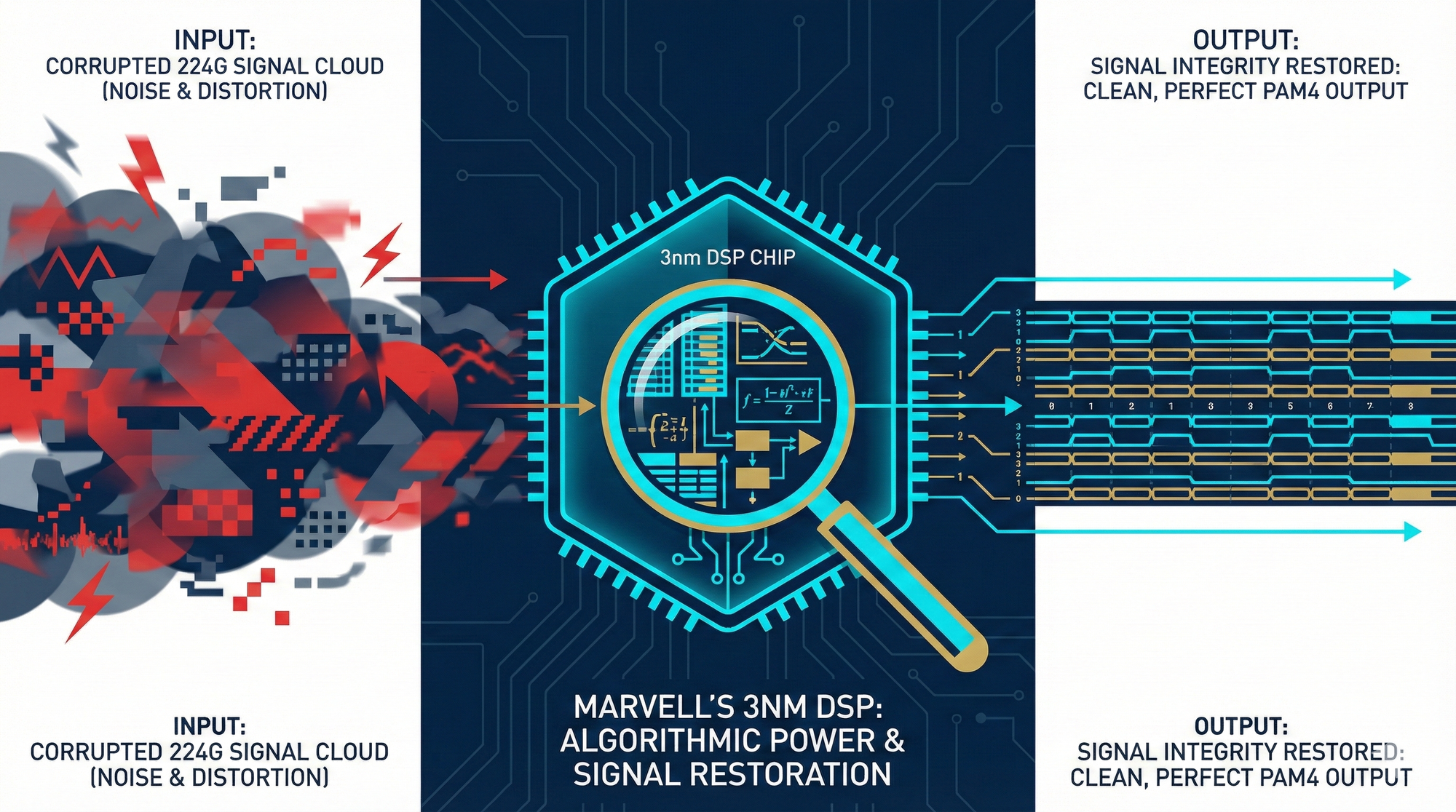

Inside an optical module, the core component, accounting for 20% to 30% of the cost, is the DSP (Digital Signal Processor). In the 1.6T era, the DSP's status has escalated from an "important component" to a "strategic bottleneck."

1. Why is the 1.6T Era Inseparable from Marvell?

When transmission rates increase to 1.6T, the underlying technology used is 8 channels, with 200G per channel (8x200G).

Physical Impossibility: At the extreme speed of 224Gbps per second, electrical signals inside motherboards or optical modules experience severe distortion. This is like trying to hear a whisper from a distance in a raging storm, where background noise completely drowns out the real signal.

The Brain's Restorative Power:Marvell, leveraging its leading edge in 5nm and 3nm process technologies, possesses DSP chips with powerful PAM4 modulation and front-end signal compensation capabilities. Through extremely complex algorithms, it can "redraw" almost destroyed noise back into a clean digital waveform within nanoseconds (ns).

2. The "Chokepoint" Power Structure: Industry Tax Collector

Currently, the global high-end optical communication DSP market is virtually monopolized by a duopoly: Marvell (after acquiring Inphi) and Broadcom.

Supply-Demand Asymmetry: Whether it's module manufacturers in Taiwan or leading manufacturers in China, if they cannot obtain Marvell's latest generation of 1.6T DSP chips, their modules will be nothing more than hot, non-communicating scrap metal.

Standard-Defining Power: Marvell not only sells chips but also co-defines 1.6T transmission protocols with cloud giants like Google and Meta. This ability to lock in customer specifications from the chip end makes Marvell one of the companies with the most "taxation power" in AI infrastructure by 2026.

3. 200G per Lane: The Physical Watershed

2026 marks the watershed year for crossing from 100G/lane to 200G/lane.

Technological Chasm: Many second-tier DSP manufacturers can stably process 100G signals, but once they jump to 200G, yield rates and Signal Integrity experience a precipitous drop.

Advanced Process Barrier: The immense power consumption generated by processing 1.6T signals forces DSPs to move to the 3nm node. Marvell's deep collaboration with TSMC ensures its leading position in the first wave of 1.6T module mass production in 2026.

📡 Chapter Two: The Laser Bottleneck — Lumentum (LITE) and the Transformation of the "Mother of Cycles"

The optical communications industry is undergoing a magnificent "species evolution." In the past, Lumentum (LITE)'s main revenue came from the slow-growing traditional telecom (Telco) and general networking markets. But by 2026, this laser giant has fully "Pivot to AI," with its core impetus shifting from traditional fiber optics to the ultra-high-speed laser technology required for AI data centers.

This post is for subscribers only

Sign up now to read the post and get access to the full library of posts for subscribers only.