💎 The Curse of Marble: The Million-Level Landmines of TGV (Through Glass Via)

Glass substrates possess impeccable physical properties, but they remain stuck in laboratories and pilot production lines, unable to achieve mass production.

The reason is a fatal physical curse: extreme fragility.

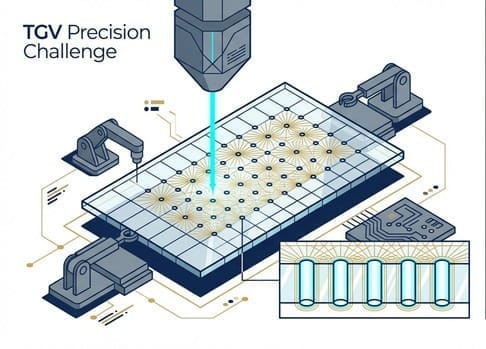

To enable electrical conduction on glass substrates, we must drill hundreds of thousands, or even millions, of holes with diameters finer than a strand of hair. This is known as TGV (Through Glass Via).

Although we mentioned in 4-1-3, there are now advanced technologies like laser modification and wet etching (LIDE) that can drill these holes.

The real "hellish bottleneck" is not whether the holes can be drilled, but rather:

After drilling millions of holes, how to ensure there are no fatal residual stresses or micro-cracks within the glass.

Imagine: Hundreds of thousands of holes densely drilled on a piece of glass as thin as a cicada's wing.

If the edge of just one of these holes develops a "nanoscale micro-crack" invisible to the naked eye during high-temperature laser irradiation.

When this glass substrate is sent into a reflow oven above 200°C to be bonded with chips at high temperatures, the thermal expansion stress will instantly concentrate on that tiny crack.

Then, in the cleanroom, you will hear a crisp "snap": the entire priceless glass substrate, along with the high-end AI chips on it, will instantly shatter into a spiderweb of scrap in the oven.

"Million-hole consistency and absolute stress control" is the greatest hurdle blocking the mass production of glass substrates.

🦅 The Grandmaster's Counterattack: Intel's Strategic Master Plan

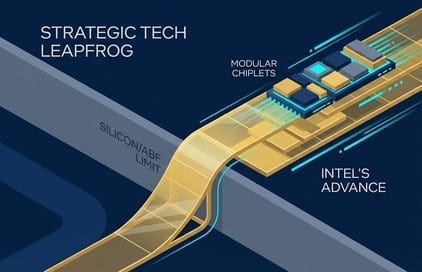

Facing this formidable challenge, why is it that Intel (US) is moving the fastest, betting the most aggressively, and even significantly ahead of TSMC?

Behind this is Intel's "strategic master plan" for a desperate counterattack.

In the wafer foundry battleground (3nm, 2nm), Intel has already acknowledged TSMC's dominant position. A direct confrontation would have very low odds of success.

However, for decades, Intel has been the grandmaster of "advanced packaging."

Intel has identified that TSMC's CoWoS and ABF plastic substrates will gradually hit their physical limits after 2026.

Intel's calculation is:

"If I can be the first to mass-produce glass substrates, I can achieve a 'cornering overtake' at the packaging level."

Intel aims to use relatively inexpensive mature-process chiplets, leveraging the extreme flatness and ultra-high-density 3D stacking capabilities of glass substrates, to assemble a super-chip whose performance can rival, or even surpass, TSMC's 2nm marvel.

To this end, Intel has quietly invested for ten years in Arizona, USA, establishing a significant glass substrate pilot production line.

🤝 This Is Not a Solo Challenge: An Alliance Battle Requiring Collaborative Effort

Intel's engineers quickly discovered a cruel truth: To break the TGV shattering curse, it absolutely cannot be solved by Intel alone or by a single equipment vendor.

- If the laser drilling machine isn't precise enough, the glass will crack.

- If the annealing temperature curve is incorrect after drilling, the glass will crack.

- If the insulating layer is applied unevenly, causing thermal stress imbalance, the glass will still crack.

This means: the mass production of glass substrates is, in essence, a highly interdependent equipment alliance battle.

Intel must tightly bind together the four forces of "laser drilling," "stress management furnaces," "precision coating," and "substrate manufacturing."

If even one party fails, the entire production line will collapse.

🛡️ The Glass Avengers Alliance: A Roll Call of the Four Critical Bottlenecks

To safely complete millions of drilling and coating operations on extremely fragile "marble" (glass), the following four Taiwanese manufacturers are almost indispensable in the current pilot production lines.

If glass is a shattering disaster, Titan Tech (8027) is the only one who can precisely defuse the bomb.

As we mentioned in 4-1-3, Titan Tech possesses the extremely critical "laser modification" technology.

Without its ultrafast laser equipment, the glass would shatter as soon as it's drilled.

Titan Tech holds the key to TGV not cracking, controlling the main artery of the process.

After laser drilling and chemical etching are completed, the glass interior is filled with volatile residual stresses.

It must then be sent into C Sun's (2467) "annealing furnace," where stringent temperature curve control is applied to allow the glass to slowly cool and release stress.

C Sun's (2467) thermal processing equipment is the ultimate insurance to ensure the glass "does not self-destruct" during subsequent processing.

On an absolutely flat glass surface, an extremely thin layer of insulating dielectric material must also be applied.

Even a single micron of unevenness in the coating could destroy the glass's flatness advantage.

Chin-Yi (6664), with its accumulated expertise in coating from PCB and FOPLP, secured the coating contract for which "microscopic flatness" is paramount.

The first three companies are equipment vendors, "selling shovels."

The one integrating the equipment, acquiring Corning's bare glass, taking on Intel's specification requirements, and bearing full responsibility for the final "yield rate" is Taiwan's leading substrate manufacturer, Unimicron (3037).

Unimicron (3037) is deeply tied to Intel behind the scenes and has already established a classified glass substrate pilot production line.

⏳ Battlefield Timeline: A Sniper Map for "Patient Capital"

Having understood the formations, the next is the most realistic question: When will profits be made? How should capital be allocated?

Glass substrates represent a "long-term fundamental restructuring." Those expecting explosive revenue next month are destined for disappointment.

Here, we outline "three investment phases" as a strategic map for patient capital.

In this phase, there's only hype, the market relies on thematic speculation, and the stock prices of any companies even remotely related to glass will surge.

However, actual revenue contribution is almost zero.

This is currently ongoing.

Intel, Absolics, and Unimicron, in order to set up their pilot production lines:

"Regardless of how poor the final yield rate may be, the equipment must be purchased first."

Therefore, **Titan Tech (8027), C Sun (2467), and Chin-Yi (6664)**, this group of "shovel-selling" equipment vendors, will be the first to experience substantial revenue and rising gross margins from high-end equipment shipments.

Investment Strategy: Heavy allocation to equipment armsmakers.

When the yield rate crosses the passing threshold, and AI servers adopt glass substrates as standard equipment, massive orders will then emerge.

At this point, the factory construction benefits for equipment vendors will slow down, but substrate giants like **Unimicron (3037)** will experience tremendous performance growth, exclusively enjoying the monopolistic benefits of the "Marble Age."

Investment Strategy: Harvesting the substrate prime contractors.

The Iron Law of the Glass Battlefield: equipment first, substrates later.

In-depth Research · Quantitative Perspective

Want to gain more insights from semiconductor quantitative research?

【Insight Subscription Plan】Bid Farewell to Retail Investor Mentality: Build Your Alpha Trading System with "Quantitative Capital Flow" and "Consensus Data"EDGE Semiconductor Research

📍 Series Map — Navigate the Complete EDGE Semiconductor Research →