Key Takeaway: This article discusses "who is defining the specifications for AI data centers" and the respective power positions of NVIDIA, OCP/Hyperscalers, system manufacturers, component manufacturers, and Vertiv/Delta Electronics.

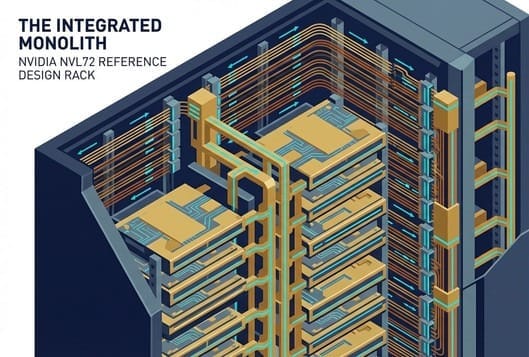

🏰 NVIDIA's Closed Empire: NVL72's "One-Stop" Dominance

NVIDIA is no longer just a chip company; it is transforming into a "data center company."

In the past, NVIDIA only sold GPUs (such as H100), while the design of server racks, power connections, and liquid cooling systems were decided by companies like Dell, HPE, or Quanta.

However, with the Blackwell GB200 NVL72 generation, everything has changed.

NVIDIA defines everything.

The NVL72 is a standardized "rack-level" product. From the Compute Tray, Switch Tray, copper backplane (NVLink Switch), to the Power Shelf and cooling manifold, all designs are drafted by NVIDIA's engineers.

This is known as the "NVIDIA Reference Design."

This has two profound implications:

- Group A Hierarchy: To ensure the operation of this sophisticated rack, NVIDIA has designated an Approved Vendor List (AVL). If you manufacture liquid cooling plates and are not in Group A, you won't even be eligible to submit a quote. This grants NVIDIA immense power over its supply chain.

- ODM Commoditization: The role of server manufacturers (such as Quanta and Foxconn) has been compressed. They no longer need to worry much about system design, as NVIDIA has handled it all. Their primary task has become "high-quality assembly and testing."

Keywords: Reference Design + AVL (Group A)

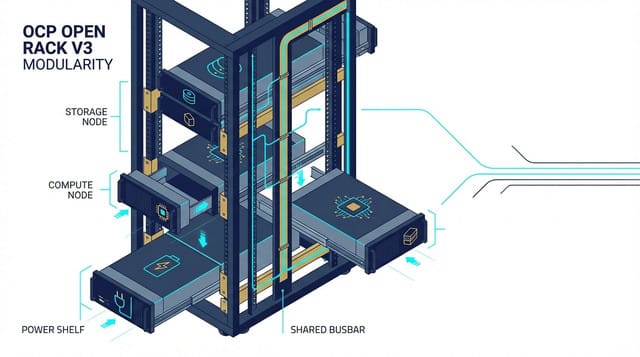

🗽 OCP's Open Alliance: The Hyperscalers' Counterattack

However, not everyone is willing to defer to NVIDIA.

Cloud giants like Meta, AWS, and Microsoft, which operate millions of servers, are most afraid of "Vendor Lock-in." If even rack specifications are dictated by NVIDIA, they risk becoming mere compute power leasing providers.

Therefore, they are vigorously promoting OCP (Open Compute Project).

OCP's core philosophy is "standardization" and "modularity."

- ORv3 (Open Rack v3): This is the standard rack specification defined by OCP. It specifies the location of the Busbar, the voltage (48V), and the width (21 inches).

- Benefits of Universality: As long as a product complies with OCP standards, whether it's a server from Wiwynn, a power supply from Delta Electronics, or a chassis from Lite-On, it can be plug-and-play. This gives Hyperscalers the power to switch suppliers at any time.

Contrast: NVIDIA pursues "closed integration"; OCP pursues "open standardization."

🇹🇼 Wiwynn (6669) 's Strategic Choice: Standing on the Shoulders of OCP

In this power struggle, Wiwynn has chosen a very unique path.

Unlike Foxconn or Quanta, which actively embrace NVIDIA's NVL72, Wiwynn tends to align with Meta and AWS.

According to the latest reports from Morgan Stanley and UBS:

- ASIC Priority: Wiwynn is a primary partner for Meta's in-house developed chip MTIA and AWS's Trainium. These ASIC servers typically adopt the OCP architecture, rather than NVIDIA's standard architecture.

- Protection of Profit Structure: The UBS report specifically noted that Wiwynn's involvement in NVIDIA GPU projects is relatively cautious (Limited ramp of NVIDIA racks), as this "buy/sell" model tends to dilute gross margins. In contrast, ASIC projects allow Wiwynn to leverage its strengths in OCP rack design and thermal integration, enjoying better profits.

- Standard Setter: As a Platinum member of OCP, Wiwynn has participated in defining the specifications for next-generation immersion cooling tanks. This gives it significant influence within the non-NVIDIA camp.

The Core of this Section: Wiwynn is not "avoiding NVIDIA" but rather placing its focus for power and profit on "OCP + ASIC + Specification Setting."

⚖️ Component Manufacturers with Dual Bets: Lotes (3533) 's Ambidextrous Approach

Compared to system manufacturers who must choose a side, component manufacturers have adopted a strategy of "playing both sides."

Take Lotes (3533) as an example:

- In the NVIDIA Camp: It strives to enter Group A for GPU Sockets and QD (quick disconnect) connectors to capture a share of the GB200 market.

- In the OCP Camp: It is the dominant player in CPU Sockets. With the recovery of the General Server market and the increasing market share of AMD EPYC processors in OCP architecture, Lotes continues to earn high-margin socket revenue steadily.

A BofA report emphasized that while the AI business is a future highlight, Lotes' current strong cash flow and profitability primarily stem from the recovery of the general server market. This demonstrates that in the specification war, manufacturers controlling core components (such as Sockets) are indispensable, regardless of which side wins.

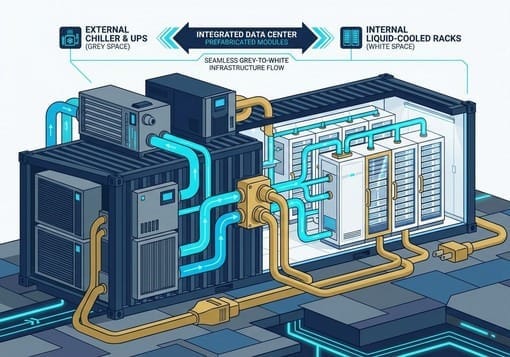

🏳️ The War of Grey and White: White Space vs. Grey Space

To understand Vertiv's dominance, one must first comprehend the two worlds of data centers:

- Grey Space (Facility Side): Refers to the infrastructure "outside" the server room, such as massive chillers, generators, UPS (uninterruptible power supply) systems, and power distribution panels. This falls under the traditional scope of mechanical and electrical engineering.

- White Space (IT Server Room Side): Refers to the area "inside" the server room where servers are placed. This includes server racks, rack-mounted CDUs, Busbars, and Rear Door Heat Exchangers (RDHx). This falls under the scope of IT equipment.

Historically, these two worlds were separate. Companies selling air conditioners didn't understand servers, and companies selling servers didn't understand air conditioners.

However, Vertiv's formidable aspect is that it is one of the very few giants capable of "dominating both grey and white."

According to the latest industry analysis, Vertiv was previously considered strong in Grey Space, but is now actively invading White Space.

Its SmartRun solution is a liquid cooling management system specifically designed for White Space. It even acquired companies like PurgeRite to complement its critical capabilities in pipeline cleaning and fluid management within White Space.

This means Vertiv can tell clients: "Just give me the land, and I'll handle all the power and cooling, from outside to inside."

In short: Vertiv's strength comes from "cross-domain integration" (from facility side to rack side), selling engineering and delivery together.

🏗️ The Victory of Prefabrication: The Ultimate Solution to "Labor Shortages"

Why is "all-inclusive" so important now? Because of "labor shortages."

In the European and American markets, finding enough skilled technicians to install complex liquid cooling pipelines on-site is both expensive and time-consuming.

Therefore, Vertiv is vigorously promoting its Prefab (prefabrication/modularization) strategy.

Imagine, instead of slowly assembling pipelines on-site like building a house, Vertiv directly assembles and tests entire power modules or cooling modules in the factory, creating a container-like block.

Once transported to the site, it's like stacking building blocks; simply connect to water and electricity, and it's ready to use.

This "system-level architecture" not only significantly shortens the data center construction cycle (Time-to-Market) but also addresses the pain point of clients lacking engineering teams to design cooling systems.

This is why Vertiv commands extremely high pricing power in the US market, because clients are buying "speed and certainty," not just products.

🤝 NVIDIA's Best Partner: High-Voltage Power and Cooling Synergy

Within NVIDIA's ecosystem, Vertiv plays an indispensable role as an "infrastructure partner."

As chip power consumption continues to rise, power architecture is undergoing a fundamental transformation. The HVDC (High-Voltage Direct Current) trend we mentioned in 6-1 is something Vertiv is already prepared for.

The latest intelligence indicates that Vertiv is about to launch a comprehensive 800V DC product portfolio, including Sidecar (side power cabinets) that support AC to DC conversion. This is entirely in preparation for NVIDIA's next-generation high-voltage architectures (such as Rubin Ultra).

Furthermore, regarding the complexity of liquid cooling systems, Vertiv emphasizes not just the CDU itself, but the overall fluid dynamics control of "how the CDU connects upwards to chillers and downwards to manifold pipes."

This "Holistic" design capability makes it a necessary consultant for NVIDIA when formulating reference designs. Because without solving cooling and power, even the most powerful GPU is just a piece of scrap metal.

🛡️ The Moat: Not Just Selling Hardware, But "Services"

Finally, we must consider Vertiv's invisible moat—Service.

Liquid cooling systems are ten times more complex than air cooling. Will the pipes leak? Does the coolant need changing? Are the filters clogged? All of these require professional maintenance.

Vertiv boasts a global service team, which allows it to continuously earn high-margin maintenance revenue after selling hardware. For cloud companies that prefer not to employ their own team of plumbers and electricians, Vertiv's one-stop service offers extremely high stickiness.

🌡️ The Convergence of Physics: When Power Supplies Also Need "Water"

Let's start with a simple physics formula: $P_{loss} = P_{in} \times (1 - \eta)$.

Even Delta Electronics, with its ultra-high conversion efficiency of 97.5% for titanium-grade power supplies, will still have a 2.5% energy loss when facing the NVL72 rack's total power consumption of 120kW.

Where does this 2.5% go? It all turns into "waste heat."

$120kW \times 2.5\% = 3kW$.

Please note, this 3000 watts of heat is not from the GPU, but from the power supply unit (PSU) itself!

In traditional servers, PSUs could be cooled simply by their built-in small fans. However, in AI racks, if 3000 watts of heat cannot be dissipated, the power supply will directly overheat and fail, leading to the collapse of the entire computing center.

Therefore, in NVIDIA GB200's architecture, we see a historic turning point: the power supply unit itself has begun to adopt "liquid cooling."

This means that those who make power supplies must also know how to integrate liquid cooling plates into high-voltage circuits without leaks or short circuits. This technical barrier instantly filters out 90% of second-tier power supply manufacturers worldwide.

High Voltage + High Heat + Liquid Cooling = Elevating supplier entry barriers to an "interdisciplinary engineering" level.

🧬 A Unique DNA: Delta Electronics' "Amphibious" Moat

In this "electrical and thermal" battlefield, Delta Electronics (2308) holds an unparalleled strategic position globally.

Let's look at its competitors:

- Lite-On Technology (2301): Strong in power supplies, but its depth of deployment in thermal management (fans/liquid cooling) is not as extensive as Delta's.

- Cooler Master (3017) / Sunonwealth Electric Machine Industry (3324): Strong in thermal management, but does not manufacture power supplies.

- Vertiv (VRT): Strong in system integration, but relies on external procurement for core power modules and fan components (partially from Delta).

Only Delta Electronics is truly a "complete entity."

It is not only the global market leader in server power supplies (market share >50%), but also a top-tier supplier of server fans and thermal modules worldwide.

This gives Delta Electronics exclusive Co-Design capabilities:

- Liquid-cooled PSU: Delta Electronics can design its own power circuits and simultaneously design the liquid cooling plates integrated within them.

- Integrated Power Shelf: It can sell to NVIDIA a super power shelf that includes a 33kW power module, Busbar, and even integrated CDU functions.

For NVIDIA or Hyperscalers, this is simply a perfect "one-stop shop." They don't need to find manufacturer A for power and manufacturer B for cooling, then worry about conflicts between the two. With Delta Electronics, everything is handled at once.

🌊 From Grid to Chip: Full-Chain Energy Dominance

Delta Electronics' ambition extends beyond the server rack. Its strategic blueprint is "From Grid to Chip."

- Grid (Grid-side): Delta Electronics has large-scale Energy Storage Systems (ESS) and microgrid technology.

- Facility (Facility-side): It offers UPS (Uninterruptible Power Supply) and large-scale data center air conditioning.

- Rack (Rack-side): It provides Power Shelves, Fan Walls, and CDUs.

- Chip (Chip-side): It supplies TLVR (inductors) and Cold Plates.

In the NVIDIA GB200 supply chain, Delta Electronics is one of the few manufacturers capable of securing both Power Shelf (power) and Cold Plate (cooling)—two critical entry tickets.

Especially in the design of Sidecar (side power cabinets), Delta Electronics has become an indispensable partner for NVIDIA due to its absolute advantage in DC-DC conversion efficiency. This is why foreign institutional investors widely believe that Delta Electronics' content value in AI servers will be 5 to 10 times that of traditional servers.

🚀 Future Outlook: A Trillion-Dollar "Energy Arms Dealer"

Looking beyond 2026, with the exponential growth in AI computing demand, power and cooling will become scarcer resources than chips themselves.

"Whoever can dissipate the most heat with the least power will be the king."

Delta Electronics is undergoing a transformation from a "component manufacturer" to an "energy solution provider."

It is no longer just selling a fan for a few hundred NT dollars, or a power supply for a few thousand NT dollars. It now sells a "thermal management system" worth tens of thousands of US dollars.

This system-level sales approach not only raises the revenue ceiling but also builds an extremely high technological moat. This is because it requires comprehensive capabilities spanning electronics, mechanics, chemistry, and fluid dynamics.

In-depth Research · Quantitative Perspective

Want more quantitative research insights on semiconductors?

【Insight Subscription Plan】Break Free from Retail Investor Mentality: Build Your Alpha Trading System with "Quantitative Chips" and "Consensus Data"EDGE Semiconductor Research

📍 Series Map — Navigate the Complete EDGE Semiconductor Research →