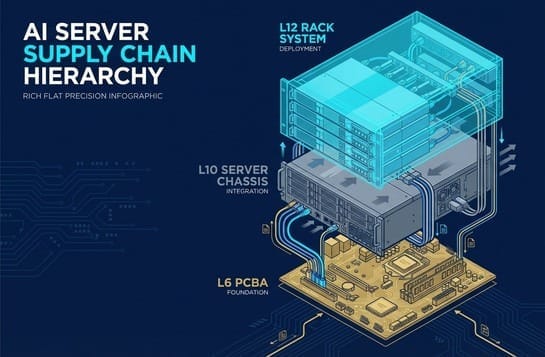

📜 The Supply Chain's 'Hierarchy': Unveiling L-Codes

To understand the profit distribution of AI servers, you must first learn the supply chain's 'jargon'. This isn't simple assembly; it's a stacking of value. The birth of a server is strictly divided into different assembly stages (Levels), with the three most critical nodes being:

- L6 (PCBA - Mainboard Assembly): This is Wistron's home turf.

- Definition: Expensive and core chips such as GPUs, CPUs, memory, and NVSwitch are soldered onto a PCB board using SMT (Surface Mount Technology) to create a fully functional 'Compute Baseboard' or 'Compute Tray'.

- Value: Extremely high. This board carries over 80% of the entire machine's cost (because 8 H100/B200 GPUs are on it).

- L10 (System - System Assembly): This is the battleground for Quanta, Wiwynn, Hon Hai (Foxconn), and Gigabyte.

- Definition: The L6 baseboard is installed into a chassis, connected to power, cooling, and hard drives, becoming a complete 'server'.

- L12 (Rack - Rack Assembly): This is the ultimate goal for Hon Hai (Foxconn) and Quanta (e.g., NVL72).

- Definition: Dozens of servers are secured into a rack, connected to switches and liquid cooling, loaded with software for testing, and finally shipped as a complete rack.

Here's the key: In the past, everyone thought L10 (complete machine assembly) was the most glamorous. But in the AI era, L6 (baseboard manufacturing) is the hidden profit generator.

Wistron seized the manufacturing rights for this 'AI heart,' becoming an indispensable 'mother' within the NVIDIA ecosystem.

🦅 Wistron (3231)'s Rebirth: Cutting Ties with Apple, Embracing NVIDIA

A few years ago, Wistron was regarded by the market as a 'second-tier contract manufacturer,' earning meager profits from its Apple iPhone assembly business. However, Wistron made a bold decision: gradually exiting low-margin consumer electronics assembly (such as selling its iPhone plant in India) and fully transitioning to the high-margin AI and server sectors.

This audacious gamble bore fruit in 2023-2024. When NVIDIA launched its HGX H100 platform, to ensure the quality of these ultra-high-density, ultra-high-unit-price GPU baseboards, NVIDIA selected Wistron as a 'Key Supplier' for L6. The latest industry data confirms the success of this transformation: Wistron's revenue in January 2026 reached NT$228.4 billion, with a year-on-year growth rate as high as 152%. This impressive growth is primarily attributed to better-than-expected shipments of GB200/300 Compute Trays.

This means that no matter whether the final AI server bears the Dell brand or the Supermicro brand, the GPU baseboard inside them most likely originated from Wistron's factories.

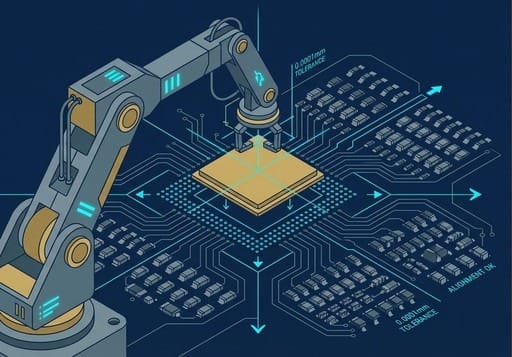

🧪 Technological Barrier: SMT's 'Zero-Tolerance' Yield Battle

Many people might ask: 'Is it really that difficult to solder chips onto a board?'

In the AI era, it is extremely difficult.

An NVIDIA HGX baseboard contains 8 GPUs, several NVLink Switch chips, and tens of thousands of passive components and power management ICs. The total value of this board can be as high as hundreds of thousands of US dollars.

If, during the SMT process, a single solder ball is not properly soldered (cold solder joint), or a tiny speck of dust causes a short circuit, this prohibitively expensive board could be rendered scrap, or require extremely costly rework.

Leveraging its accumulated automated optical inspection (AOI) and process capabilities in the server domain, Wistron maintains extremely high yield rates. This is not merely labor-intensive; it is 'precision manufacturing.' It is precisely this mastery of yield control that has built its moat in the L6 sector.

💰 Metamorphosis of Profit Structure: The Myth of Gross Margin and the Truth of Profitability

Investors often have a misconception: why does Wistron's Gross Margin (GM) sometimes decline? According to the latest report, Wistron's GM for Q4 2025 was approximately 5.62%, slightly below expectations. However, this is actually a 'good problem to have'.

This is because the unit price of AI servers (especially GPU baseboards) is exceedingly high. As Wistron ships more AI baseboards, the revenue denominator is inflated by the expensive GPUs, causing the gross margin percentage to appear diluted. However, if we look at 'Operating Profit Margin (OPM)' and 'absolute profit amount,' the situation is entirely different. With the increasing proportion of AI products (AI servers are expected to contribute 76%~85% of gross profit from 2025-2027), Wistron's core business profitability is undergoing a structural improvement. As economies of scale expand and production efficiency increases, Wistron's core business (excluding its subsidiary Wiwynn) operating profit margin will continue to expand.

Wistron's current strategy is crystal clear: it doesn't necessarily need to compete in the red ocean of the final bulky rack assembly (L12). By firmly holding its position in the L6 segment, it can enjoy the sweetest and purest dividends of AI growth.

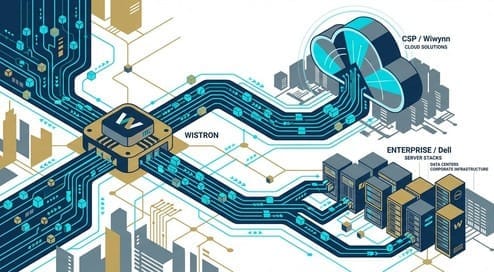

🤝 Perfectly Complementary Dual Engines: CSP and Enterprise's Complementary Interplay

Observing the Wistron Group's strategic layout, it must be seen as a 'dual-arrow' strategic combination. This allows it to cover all end-user demands for AI servers and diversify single-market risks:

- Left hand seizes CSPs (Cloud Giants): Through its subsidiary Wiwynn, Wistron indirectly secures orders from hyperscale data centers like Meta and AWS. This segment operates under an ODM Direct model, with specific specifications and high reliance on customized ASICs.

- Right hand targets Enterprise (Enterprise-grade): The parent company, Wistron, directly engages, leveraging its strong L6/L10 manufacturing capabilities to deepen cooperation with branded manufacturers such as Dell.

Strategic Insight: As AI technology matures, demand will spill over from the 'training end (CSP)' to the 'inference end (Enterprise).' The latest industry intelligence indicates that despite the traditional off-season for the laptop market, Wistron's revenue has managed to hold steady or even grow against the trend, primarily driven by Dell's robust demand for AI server racks. This proves that the enterprise-grade market is awakening, and Wistron has precisely positioned itself.

📈 January 2026 Mass Production Signal: The Explosion of GB200/300 Compute Tray Shipments

The data is honest. Wistron's year-on-year revenue growth rate in January 2026 reached an impressive 152%. Behind this astounding figure lies a critical development in NVIDIA's next-generation architecture:

- Compute Tray Volume Ramp-up: Industry supply chains confirm that this surge is not accidental, but rather a result of GB200/GB300 Compute Tray shipments significantly exceeding expectations. This indicates that NVIDIA's Blackwell platform has overcome initial mass production bottlenecks and officially entered its ramp-up phase.

- Surge in Shipment Scale: Based on shipment data projections, monthly shipments of rack equivalents have significantly increased compared to the previous month, demonstrating extremely strong pull-in momentum from downstream customers.

- Full-Year Outlook: Based on this momentum, the industry generally expects Wistron's AI server revenue for 2026 to double compared to 2025. This represents not only an increase in volume but also a value enhancement driven by product generation shifts.

🛡️ Supply Chain's 'Mother' Status: Controlling the Outlet from the Source

To summarize Wistron's special position in the AI industry chain: it is the 'source of AI computing power'.

Within NVIDIA's supply chain ecosystem, L6 (GPU baseboards) is the segment with the highest technical barrier and the strictest certification. Wistron has successfully positioned itself as the primary supplier for this segment.

This signifies an interesting industry phenomenon: regardless of which downstream company is assembling the complete machine (Hon Hai (Foxconn), Quanta, or Supermicro), the most expensive and core compute baseboard inside them most likely originates from Wistron's factories.

This 'locking down the source' strategy grants Wistron extremely high strategic security and bargaining power. As long as the global total volume of AI servers grows, Wistron will invariably be among the first beneficiaries, and its profit structure will continue to optimize as the proportion of AI products increases.

In-Depth Research · Quantitative Perspective

Want to gain more insights from semiconductor quantitative research?

【Insight Subscription Plan】Say Goodbye to Retail Investor Mindset: Build Your Alpha Trading System with "Quantitative Fund Flows" and "Consensus Data"EDGE Semiconductor Research

📍 Series Map — Navigate the Complete EDGE Semiconductor Research →