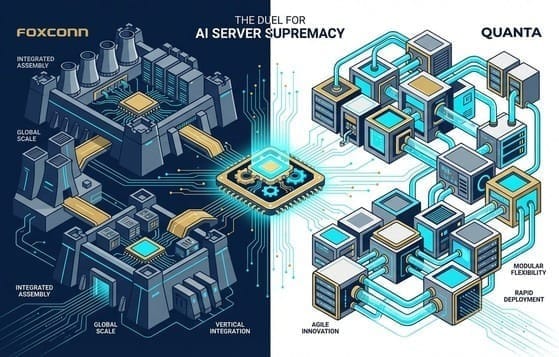

Key Takeaways (Original text preserved, only formatted)

- Hon Hai's core strengths: 80% in-house production rate + automated replication capability + US production capacity expansion → Scale advantage for GB200/NVL72 (Beta)

- Quanta's core strengths: Proficiency in MGX architecture + QCT's R&D speed + Deep ties with Google/Meta → Customization and first-wave orders (Alpha)

- 2026 Supply & Demand Context: CSP Capex revised up to $676.4 billion, with approximately 60% allocated to data centers/servers → Extended order visibility

🏰 The Pinnacle of Vertical Integration: The Ambition of 80% In-house Production Rate

To understand the formidable strength of Hon Hai in the GB200 era, one must look beyond its assembly lines and delve into its BOM (Bill of Materials).

In traditional servers, assembly plants earn meager processing fees (MVA). But in AI servers, Hon Hai has activated a group-wide operational model.

Section Summary: Hon Hai upgrades "assembly" into a "group supply chain" profit integrator.

According to the latest industry research, Hon Hai has set an aggressive target for the non-chip BOM of AI server racks: 80% of components are to be manufactured in-house by the group. This includes:

- Mechanical components: Chassis, rack structures (supported by subsidiaries Hon Teng and Eslung).

- Thermal solutions: Liquid quick disconnects (UQD), manifolds, and even cold plates.

- Connectors and cable assemblies: High-speed connectors, copper cables (supported by subsidiary FIT Hon Teng).

- Power: Power supplies and busbars.

This "one-stop-shop" strategy offers two major strategic advantages:

- Cost Moat: While others still purchase UQD quick disconnects from suppliers, Hon Hai manufactures its own. This gives it enormous flexibility in pricing while maintaining the group's overall gross margin.

- Supply Chain Resilience: In the AI era, where material shortages are common, in-house manufacturing means "not being bottlenecked." This is a huge incentive for NVIDIA and CSP customers who are in a hurry to ship products.

🤖 Manufacturing as a Service (MaaS): The Victory of Automation and US Capacity

NVIDIA CEO Jensen Huang once mentioned that the simplified design of the new-generation Vera Rubin platform will drastically cut assembly time from several hours for GB200 to just a few minutes. This might sound like lowering the barrier, but in reality, it rewards manufacturers with strong "automation capabilities."

Section Summary: Simplified design does not mean lower barriers, but rather that success depends on automation and production transfer capabilities.

Hon Hai is indeed the king of automation. Leveraging its deep roots in smart manufacturing, it can rapidly replicate production lines. More importantly, Hon Hai is undergoing a "major production capacity migration":

- Made in USA: In response to "Sovereign AI" and geopolitical demands, Hon Hai is vigorously expanding its US production capacity. Industry intelligence suggests that by the end of 2025, the US is expected to surpass Mexico as Hon Hai's largest AI server production base, accounting for over 50% of its total capacity.

- Production Scale: Hon Hai's current AI server production capacity is approximately 1,000 racks per week, projected to double to 1,500 to 2,000 racks per week by the end of 2026. This scale is unattainable for other second-tier manufacturers.

🌊 The Key Battle of Liquid Cooling Technology: From UQD to NVQD

In the GB200 and future GB300/VR200 generations, thermal management technology is a core battleground.

Hon Hai not only performs assembly but also delves deep into the R&D of critical liquid cooling components.

Section Summary: Evolution of liquid cooling interface specifications = New entry point for component profits and patent binding.

According to supply chain intelligence, the thermal design of the Switch Tray in current GB300 racks has become more complex, with an increased number of cold plates. In the next-generation VR200 (Vera Rubin) platform, thermal management will shift entirely to "full liquid cooling," with cold plates covering GPUs, CPUs, and SOCAMM memory modules.

The evolution of liquid cooling connectors is noteworthy:

- GB200/300 Generation: Primarily uses universal standard UQD (Universal Quick Disconnect).

- VR200 Generation: Expected to largely transition to NVIDIA's custom NVQD specification (potentially accounting for 90%).

Leveraging its deep collaboration with NVIDIA, Hon Hai has already laid out its strategy for patents and manufacturing of these critical interfaces. This means it will not only earn assembly fees but also component profits from every liquid cooling connector.

📉 2026 Strategic Outlook: The Beta Value King of GB200

To summarize Hon Hai's strategic position: it is the Beta value (representing market aggregate) of GB200. Industry estimates project Hon Hai to maintain a market share of over 40% in the AI server assembly market (including GPUs and ASICs).

Section Summary: Hon Hai's conditions for victory are "overall market expansion" and "factory operational speed."

This implies that as long as the global AI server pie grows larger, Hon Hai will be the biggest beneficiary. It doesn't need to bet on which CSP will win (although it is a major supplier to Microsoft and Oracle); it just needs to ensure its factories operate faster than others and its in-house component production rate is higher, allowing it to generate astonishing absolute profits through its massive revenue scale.

⚡ The Victory of Speed: MGX Architecture and QCT's Agile Strategy

Unlike Hon Hai's pursuit of a vast, vertically integrated fleet model, Quanta is more akin to a well-equipped "special forces unit." Its core competitiveness lies in its QCT (Quanta Cloud Technology) team.

Section Summary: MGX turns hardware into building blocks, making speed the strongest moat.

In the AI server market, specifications change extremely rapidly. NVIDIA releases H100 today, H200 tomorrow, and GB200 the day after. Quanta's advantage lies in its high proficiency with NVIDIA MGX (Modular Grid Architecture). MGX allows manufacturers to quickly mix and match different CPUs, GPUs, and DPUs like building blocks. This enables Quanta to deliver mass-producible prototypes in the shortest possible time, tailored to the specific needs of CSP customers (e.g., specialized cooling ducts, unique power backplanes).

This is why Quanta is always in the "first wave":

- When NVIDIA launches new-generation products, Quanta is often among the launch partners.

- This "R&D speed" is itself a competitive moat, because for CSPs racing against time to train AI models, receiving machines a month later could mean losing the entire model war.

🤝 CSP's Top Choice: Deep Ties with Google and Meta

If Hon Hai is the dominant player for standard GB200 products (such as NVL72), then Quanta is the king of CSP customized projects.

Section Summary: Quanta's strength lies in JDM and customer stickiness, not in pursuing maximum production capacity.

According to the latest supply chain shipment data analysis, Quanta holds a significant advantage in its supply share to major CSPs:

- Google's Number One Partner: Quanta has long held exclusive assembly for Google's TPU servers and accounts for 60%~70% of Google's AI server supply. With Google's capital expenditure projected to surge in 2026, Quanta is a direct beneficiary.

- Major Supplier for Meta and AWS: In Meta's supply chain, Quanta accounts for approximately 40%; for AWS, it also accounts for about 40%. These customers tend to adopt highly customized rack designs (such as AWS's customized NVL36), which is a strong suit for Quanta's JDM (Joint Design Manufacturing) model.

- Critical Supplier for Oracle: Although Hon Hai has secured most Oracle orders, Quanta still shares some high-end projects for Oracle and Microsoft, maintaining a balanced customer structure.

🚀 2026 Momentum: GB200/300 Volume Ramp-Up Signals

Quanta's growth momentum for 2026 has already ignited. The latest January revenue data shows that while notebook shipments declined due to seasonality, overall revenue year-over-year growth still reached a high of 62%. The driving force behind this comes entirely from the volume ramp-up of AI server racks.

Section Summary: Strong performance in off-season + Q1 volume ramp-up verifies the profit quality of "first-wave orders."

- Off-season Rack Shipments Exceeding Expectations: Industry intelligence estimates that Quanta shipped approximately 1,400 racks of GB200/300 servers in January.

- Q1 Explosion Expected: As supply chain material conditions ease, Quanta's AI rack shipments are projected to surge to 4,000 racks in Q1 2026, a 12% quarter-over-quarter increase.

- Profit Quality: Quanta's strategy is to "pick and choose orders." It doesn't necessarily aim to be the market share leader like Hon Hai, but it targets first-wave orders with better gross margins and higher technological content. This makes its profit structure healthier than assembly plants that simply compete on price.

🌊 Flood of Capital: A $670 Billion Arms Race

Let's look directly at the numbers. The market originally anticipated a slowdown in CSP capital expenditure growth for 2026, but the latest industry survey completely refutes this argument. The total capital expenditure of the four major US-based CSPs for 2026 is projected to be revised upwards to $676.4 billion, with the year-over-year growth rate jumping from the initially estimated 32% to 64%.

Section Summary: Capex revision upward = Order visibility extends to 2027.

Who is leading the charge?

- Google (The Biggest Accelerator): Google's 2026 capital expenditure is expected to reach approximately $180 billion, with a year-over-year growth rate as high as 97%. This is to support its TPU ASIC chip and DeepMind's computing power requirements. This is a super positive for Quanta, which has long been the exclusive supplier for Google's orders.

- Amazon (AWS Expansion): Amazon is expected to see a 52% year-over-year increase, reaching $200 billion. The focus is on expanding AWS's generative AI computing capabilities and in-house developed chips (Trainium).

- Meta & Microsoft: Meta anticipates a 65-94% year-over-year increase, while Microsoft, despite its already high base, maintains steady growth, with stronger growth momentum in FY1H26 (second half of 2025) than in the first half. These two are major markets shared by both Hon Hai and Quanta.

Strategic Interpretation: This is not just quantitative growth, but also a guarantee of "quality." A very high proportion of these funds (approximately 60%) is specifically allocated to server and data center construction. This means that Hon Hai's and Quanta's order visibility already extends directly to 2027.

💎 Transformation of Profit Structure: From "3-4% Gross Margins" to an Explosion of "Absolute Profit"

In the past, electronics contract manufacturers were often criticized for "low gross margins." However, in the era of AI servers, we must change our evaluation logic: "High ASP x Large Scale = Astonishing Absolute Profit Amount."

Section Summary: Gross margin is not the core; the core is "how much absolute profit can be earned per rack."

- The Magic of Average Selling Price (ASP):

An NVL72 rack can cost up to $3 million. Even if an assembly plant's gross margin is only 3-5%, the "absolute amount" of profit earned is tens of times that of traditional servers.

- Hon Hai's "Vertical Integration" Dividend: Hon Hai's strategy is not just to earn assembly fees. It aims for an 80% in-house production rate for its non-chip BOM. By manufacturing its own chassis, liquid cooling connectors, and power modules, Hon Hai can push up the group's overall profit margin. This is why Hon Hai has the confidence to claim a market share of over 40% in the AI server assembly market.

- Quanta's "ASIC" Dividend: Quanta is deeply involved in ASIC servers such as Google TPU and AWS Trainium. Compared to NVIDIA's standard products, which have transparent pricing, highly customized ASIC projects typically enjoy better profit margins and customer stickiness.

🥊 The Dual Champions' Final Positioning: The Choice of Alpha vs. Beta

Finally, let's position these two companies on the 2026 battlefield:

1. Hon Hai (2317): The Beta Value of AI Servers (Defender of Market Scale)

- Keywords: Scale, Vertical Integration (In-house), US Capacity.

- Strategy: Hon Hai leverages its vast global supply chain and automation capabilities to become NVIDIA's most reliant "capacity reservoir." With the expansion of US production capacity, it will become the main force satisfying North American geopolitical demands in 2026.

- Conclusion: As long as the total AI market grows, Hon Hai is the biggest winner.

2. Quanta (2382): The Alpha Value of AI Servers (The Special Forces of Technical Leadership)

- Keywords: Speed, MGX, CSP Customization.

- Strategy: Quanta utilizes QCT's R&D speed to seize market share immediately upon the launch of every new architecture (such as MGX, GB200). Its deep ties with Google/Meta give it a unique moat in the ASIC domain.

- Conclusion: If you are bullish on CSP self-developed chips and rapidly iterating technological trends, Quanta is the top choice.

In-depth Research · Quantitative Perspective

Want more semiconductor quantitative research insights?

【Insight Subscription Plan】Break Free from Retail Investor Mindset: Build Your Alpha Trading System with "Quantitative Chips" and "Consensus Data"EDGE Semiconductor Research

📍 Series Map — Navigate the Complete EDGE Semiconductor Research →