Key Takeaways

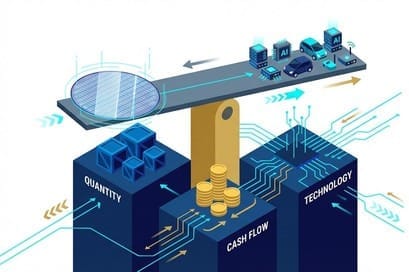

- The value proposition of channel partners: Solving the three major mismatches in quantity / cash flow / technology → "Break-bulk and consolidation + Banking + FAE"

- The "Reservoir Theory" in the AI era: Stabilizing the supply chain with inventory and fulfillment capabilities amidst severe supply-demand fluctuations.

- WPG Holdings: Profit over Share + LaaS servitization + organizational restructuring (four sub-groups → dual engines) → Defensive reservoir

- WT Microelectronics: Data center/ASIC penetration + Future acquisition barbell strategy → Offensive reservoir

- 2026 Dashboard: Using DOI (Days on Hand) to determine the recovery cycle and entry points.

🏗️ Reason for Existence: Solving the "Three Major Mismatches" Between Original Manufacturers and Customers

Many people ask: "Why doesn't NVIDIA sell chips directly to Foxconn? Why is there a WT Microelectronics or WPG Holdings in between?"

Intuitively, disintermediation seems to save costs. However, in the semiconductor industry, there are three difficult-to-bridge gaps between original manufacturers (upstream) and manufacturing plants (downstream), which is the value proposition of channel partners:

Section Summary: Channel partners are not just transporters; they are balance sheet and technical service providers that "balance" the three types of supply chain mismatches.

- Quantity Mismatch:

- Original manufacturers (e.g., Infineon): To pursue wafer fab utilization rates, they must engage in "large-scale mass production."

- Customers (e.g., Quanta): To pursue inventory turnover, they desire "small quantities, high variety, and Just-in-Time inventory."

- Role of channel partners: "Break-bulk and consolidation." They act as a large buffer, absorbing the massive output from original manufacturers and then distributing it in batches according to customer demand.

- Cash Flow Mismatch:

- Original manufacturers: R&D and factory construction are cash-intensive, so they prefer to "receive cash as soon as goods are shipped."

- Customers: They only receive payment after their products are built into servers and sold to Google, so they desire "longer payment terms (90-120 days)."

- Role of channel partners: "Bank." Channel partners use their balance sheets to cover this cash flow gap, which is why their debt ratios are typically higher—it's the nature of their business.

- Technical Mismatch:

- Original manufacturers: They only know how to design chips, but not necessarily how to "use" them in a myriad of end products.

- Customers: They need someone to teach their engineers how to use this PMIC (Power Management Integrated Circuit) in the latest AI servers.

- Role of channel partners: "FAE (Field Application Engineer)." They provide technical support and reference designs to accelerate customer product launches.

💧 Reservoir Theory: The Supply Chain Stabilizer in the AI Era

In the AI era, this regulatory function becomes even more critical. We call it the "Reservoir Theory."

The complexity of the AI supply chain is rising exponentially. SKUs (Stock Keeping Units) are surging, product iteration cycles are shortening, component specialization is increasing, and even severe raw material shortages frequently occur. Just as climate change leads to alternating heavy rainfall and droughts, AI demand is also volatile (e.g., GPU shortages but oversupply of general-purpose chips).

Section Summary: Channel partners transform supply and demand fluctuations into manageable inventory and fulfillment rhythms through "water storage/release."

IC channel partners are the "reservoirs" on this river:

- High-water season (oversupply): Channel partners store water (build inventory), preventing original manufacturers' production lines from halting and avoiding chip price collapses.

- Low-water season (undersupply): Channel partners release water (deplete inventory), ensuring uninterrupted supply for downstream assembly plants.

According to the latest industry analysis, as AI business expands, the market severely underestimates the demand for "logistics and distribution management." Especially in the ASIC (Application-Specific Integrated Circuit) sector, supply chain logistics execution capability will become the new competitive differentiator.

🛡️ Breakwater Against the Bullwhip Effect: From "Trading" to "Service"

In the past, channel partners were regarded as low value-added "transporters," with gross margins consistently suppressed at 3-4%.

However, this role is now undergoing a qualitative change. To combat supply chain fluctuations (the bullwhip effect), channel partners are beginning to offer more in-depth services:

Section Summary: Servitization is the primary path for channel partners to break through the 3-4% gross margin ceiling.

- LaaS (Logistics as a Service): It's not just about selling chips, but transforming warehousing, logistics, customs clearance, and other aspects into a "subscription-based service." This allows channel partners to shift from merely earning price differences to earning stable service fees, thereby optimizing their gross margin structure.

- Supply Chain Finance:

Leveraging industry insights to accurately assess inventory value and provide financing services to small and medium-sized customers, earning interest differentials.

⚖️ Profit over Share: WPG Holdings' "Refusal" Philosophy

Observing WPG Holdings' latest financial report, you will notice an interesting "divergence" phenomenon:

Weak revenue, but gross margin (GM) hit a new high.

According to the latest quarterly data, WPG Holdings' revenue declined by approximately 6% year-over-year, underperforming peers; however, its gross margin rose against the trend to 4.03%, exceeding market expectations. This is no accident but a carefully calculated strategic choice.

Section Summary: The key in the channel industry is not the largest turnover, but "product mix + pricing discipline."

The Dilemma of Channel Partners:

In the semiconductor channel industry, there is often a dilemma: to gain market share (especially with large orders like data centers), one often has to accept extremely low gross margins; to preserve gross margins, one must forgo some low-profit turnover.

Competitors' Choices: Other major players in the market (such as U.S.-based Arrow, Avnet, and WT Microelectronics in Taiwan) have chosen to "grab revenue" in recent quarters. They actively entered the extremely thin-margin Data Center and Server businesses, and while their revenue figures looked good, their gross margins faced significant downward pressure.

WPG Holdings' Choice: WPG Holdings chose a different path. The report analysis indicates that WPG Holdings deliberately "optimized its product mix" and "adhered to pricing discipline." This means that when faced with certain AI server bids that, while high-volume, offered razor-thin gross margins, WPG Holdings likely chose to "decline" them. It preferred to let revenue temporarily decline rather than compromise its profit bottom line. This indicates that this leading enterprise has moved beyond the stage of blindly pursuing scale and has entered a mature phase of seeking "earnings quality."

🚚 LaaS (Logistics as a Service): The Invisible Cash Cow

If "cherry-picking orders" is defense, then LaaS (Logistics as a Service) is WPG Holdings' secret offensive weapon.

For traditional channel partners, logistics costs are "expenses," but in WPG Holdings' view, logistics is a "commodity."

WPG Holdings leverages its extensive warehousing system and digitalization capabilities to separate logistics services and sell them to customers and original manufacturers. This is LaaS.

Section Summary: LaaS transforms "cost centers" into "profit centers" and drives gross margins to stabilize at 4%+.

Strategic Value of LaaS:

- High Profitability: According to industry data, while WPG Holdings' LaaS-related revenue currently accounts for a small proportion, it is growing extremely fast (up 17% year-over-year). Even more impressively, it drives a 69% year-over-year increase in Net Profit. This confirms that LaaS is a high-margin service model.

- GMV (Gross Merchandise Value) Mindset: Through LaaS, the value of goods handled by WPG Holdings (GMV) reached USD 23.9 billion. While not all of these goods are necessarily counted as revenue, every batch of goods passing through WPG Holdings' warehouses contributes service fees.

- Gross Margin Optimizer: The expansion of LaaS business is a key driver for WPG Holdings' overall gross margin to stabilize at 4% and even move upward. It allows WPG Holdings to shift from simply earning "price differences" to earning "management fees."

🧬 Organizational Restructuring: Four Sub-Groups Become Dual Engines

In addition to business model innovation, WPG Holdings has undertaken its largest organizational restructuring in recent years.

In the past, WPG Holdings had four sub-groups: WPI, SAC, AIT, and YOSUN. While this "climbing the mountain together" model was flexible, it also led to issues of duplicated resource allocation.

Section Summary: The essence of restructuring is "economies of scale + logistics integration," providing an organizational foundation for the profit-first strategy.

Latest Restructuring Plan:

WPG Holdings initiated strategic share swaps, restructuring its four business units into "two core engines":

- WPI: Maintains its flagship status within the group, directly controlled by WPG Holdings.

- AIT: Through share conversion, acquired 100% equity in YOSUN and SAC. In the future, AIT will become a super sub-group, overseeing the resources of these three entities.

Strategic Significance:

- Maximizing Economies of Scale: Post-restructuring, AIT's revenue scale will exceed hundreds of billions, enabling more effective integration of logistics, IT, and warehousing resources, thereby reducing operating costs.

- Bargaining Power with Original Manufacturers: Centralized procurement and management help deepen cooperation with international semiconductor original manufacturers (e.g., MediaTek, Realtek, Novatek, etc.).

- Efficiency Improvement: This is a classic "trimming fat and building muscle" approach. By reducing internal attrition, overall operational efficiency is enhanced, which also serves as the organizational foundation supporting its profit-first strategy.

🔮 Future Outlook: Edge AI and Inventory Optimization

Looking ahead to 2026, while WPG Holdings' aggressiveness in Cloud AI servers is not as strong as WT Microelectronics', its strategic positioning in Edge AI is very solid.

Section Summary: Edge AI is the home ground for WPG Holdings' represented product lines, complemented by inventory optimization to drive the recovery of traditional businesses.

- Opportunities in Edge AI: As AI applications move from the cloud to edge devices (such as AI PCs, AI smartphones, automotive applications), this is precisely the home ground for WPG Holdings' represented product lines (e.g., NPUs, MCUs, sensors). The company is actively introducing new related product lines, providing vertically integrated services from chips to solutions.

- Inventory Cycle Bottoming Out: Industry reports indicate that inventory adjustments in the consumer electronics and European/American industrial/automotive markets are nearing completion, with inventory levels returning to healthy levels. This means that traditional businesses, acting as "cash cows," will see a cyclical recovery in 2026.

🧬 Genetic Mutation: A Qualitative Shift from Consumer Electronics to Data Centers

In the past, investors often perceived WT Microelectronics as a "transporter of mobile phone and PC components." Such businesses are high-volume but deeply affected by consumer economic cycles.

However, according to the latest industry structural analysis, WT Microelectronics' revenue landscape is undergoing dramatic shifts.

Section Summary: WT Microelectronics' stock price correlation is shifting from consumer electronics to CSP Capex and the data center cycle.

Dominance of Data Centers: Data shows that WT Microelectronics' revenue contribution from data centers and servers is climbing at an astonishing rate. Industry projections estimate this segment's revenue contribution will soar from 42% in 2025 to 64% by 2028. This means that WT Microelectronics' future stock price correlation will shift from "mobile phone shipments" to "CSP capital expenditures."

This is more than just selling a few CPUs or memory modules. As AI server architectures become more complex (e.g., NVL72), the number of peripheral chips required (PMICs, switches, retimers, optical communication components) has surged. With its extensive product line (line card), WT Microelectronics has become an indispensable "one-stop shop" supplier for AI server BOMs.

🌪️ Deep into the Eye of the Storm: Penetrating the CSP ASIC Supply Chain

WT Microelectronics' most impressive strategy is its successful penetration into the ASIC (Application-Specific Integrated Circuit) supply chain.

Section Summary: The key to the ASIC supply chain is not design, but fulfillment capabilities in logistics, distribution, customs clearance, and cash advances.

Why do ASICs need channel partners?

You might ask: Google or AWS designs its own chips, contracts TSMC for manufacturing, and Quanta for assembly, so why do they need WT Microelectronics in between?

The answer lies in "Logistics" and "Fulfillment."

CSPs (cloud giants) are software companies; they are not adept at managing physical chip inventory and cross-border logistics. From the time chips leave the wafer fab until they are delivered to the ODM factory for assembly, complex customs clearance, warehousing, distribution, and cash advances are involved.

WT Microelectronics assumes this role. It has become the "master distributor" for ASIC chips.

Strategic Value:

- Following the Winners: With ASIC shipments projected to increase by over 50% year-over-year in 2026 (especially for Google and AWS), WT Microelectronics has directly boarded this high-speed train.

- High Stickiness: ASICs are an exclusive business; once integrated into the supply chain, it's difficult to be replaced. This provides WT Microelectronics with extremely high revenue visibility.

- ASIC Revenue Contribution: According to industry intelligence, ASIC-related business already accounted for 26.4% of WT Microelectronics' revenue in 2024, and this proportion is expected to continue expanding with AI trends.

🌍 Future Acquisition: A Perfect "Barbell Strategy"

Even without considering AI, WT Microelectronics' acquisition of Future Electronics holds significant strategic importance. This is a textbook example of a complementary acquisition, forming a perfect "Barbell Strategy":

Section Summary: Left end focuses on volume (high turnover in Asia), right end focuses on profit (high gross margin in European/American industrial control and automotive sectors).

- Left End (Original WT Microelectronics): Specializes in Asian markets, consumer electronics/computing, high turnover/low gross margin. This forms the "volume base."

- Right End (Future): Specializes in European/American markets, industrial control/automotive, low turnover/high gross margin. This is the "source of profit."

Acquisition Synergies to Materialize in 2026:

- Completing the Global Puzzle: Future provides WT Microelectronics direct entry into the European and American industrial control markets, significantly reducing its reliance on a single Asian market.

- Pricing Power: Future possesses strong pricing power in the industrial control market (due to a diverse and fragmented customer base that is less price-sensitive), which helps elevate WT Microelectronics' overall blended gross margin.

- Inventory Destocking Concludes: The report indicates that Future's revenue began to rebound from Q4 2024, signaling the end of inventory adjustments in the European and American industrial control markets. In 2026, this high-margin engine will reignite, forming a dual-engine drive with the AI business.

📈 2026 Battle Simulation: High-Growth Attacker

Overall, WT Microelectronics' strategic positioning in 2026 is very clear: it is an "attacker" in the semiconductor channel industry.

Section Summary: Growth momentum comes from the ramp-up of AI ASICs, and profit momentum comes from acquisition integration and the recovery of high-margin businesses.

- Revenue Momentum: Benefiting from the ramp-up of AI ASICs and the structural growth in data center demand, WT Microelectronics' revenue growth rate is expected to significantly outperform the industry average (estimated 2025-2028 CAGR of 20%).

- Profit Leverage: With expense integration and improved operational efficiency (Operating Leverage) post-Future acquisition, coupled with the recovery of high-margin industrial control businesses, WT Microelectronics' profit growth rate has the potential to outpace revenue growth.

- Risks and Opportunities: While high leverage (debt incurred from the acquisition) was once a market concern, the balance sheet is rapidly being repaired with strong cash flow generation.

🏁 7-3 Sector Summary: Two Types of Reservoirs

We have completed an in-depth analysis of WPG Holdings and WT Microelectronics.

While both companies operate as "channel partners," their core identities are entirely different:

Section Summary: WPG Holdings leans defensive (servitization + gross margin protection), while WT Microelectronics leans offensive (AI + M&A + market share expansion).

- WPG Holdings (3702): A stable, defensive reservoir. Earns stable service fees through LaaS, prioritizes profit over revenue, suitable for capital seeking high dividend yields and low volatility.

- WT Microelectronics (3036): An aggressive, offensive reservoir. Pursues extreme growth and market share expansion through acquisitions and heavy investment in AI ASICs, suitable for capital seeking capital gains and industry trend dividends.

Final Strategic Dashboard:

In the 2026 semiconductor recovery cycle, you can use Days on Hand (DOI) as a leading indicator to determine entry points. Currently, the DOI for non-AI products has dropped to healthy levels, meaning that beyond the AI craze, we are about to usher in a comprehensive economic rebound.

In-depth Research · Quantitative Perspective

Want more quantitative research insights on semiconductors?

【Insight Subscription Plan】 Bid Farewell to Retail Investor Thinking: Build Your Alpha Trading System with 'Quantitative Capital Flows' and 'Consensus Data'EDGE Semiconductor Research

📍 Series Map — Navigate the Complete EDGE Semiconductor Research →