Weekly Capital Market Analysis

The market showed a healthy rotation at high levels this week. After a moderate adjustment of capital from large-cap weighted stocks, funds quickly shifted into the AI server supply chain supported by strong fundamentals, with the PCB and ABF substrate groups being most favored by Foreign Institutional Investors. Meanwhile, Domestic Fund Managers continued to lead the offensive in domestic semiconductor equipment, while some Speculative Capital began to ignite interest in consumer electronics and networking groups with lower bases, creating a pattern of multi-point gains. The overall market trend shifted from a single main line of attack into a dual-track structure where the "Main AI Battlefield" and "Satellite Catch-up Units" coexist.

Our core discipline is simple: don't guess bottoms, don't predict laggard rallies. Our sole task is to use quantitative models to capture the leaders with the strongest momentum and trends in the market. To this end, we divide the market into three liquidity battlefields:

Tier 1 (Top 1-50 Liquidity) is the macro main battlefield for Foreign Institutional Investors, with long decision cycles and large capital scales;

Tier 2 (Top 51-400) is the backbone industrial battlefield for Domestic Fund Managers, focusing on industry trends and chip concentration;

Tier 3 (Top 401-1000) is the game battlefield for local capital and short-term Speculative Capital, where themes and event-driven factors are king.

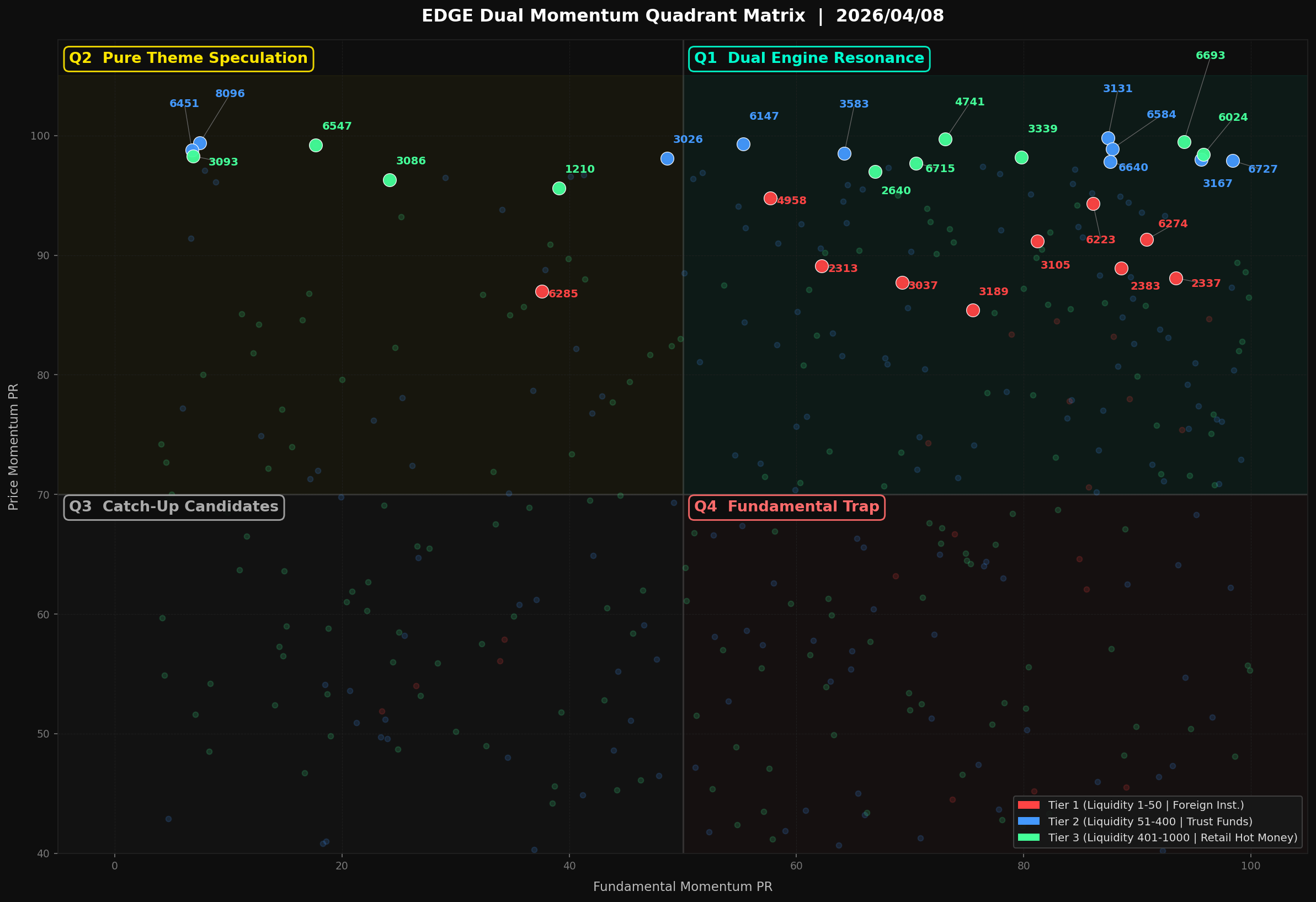

All targets will be projected onto the EDGE Dual-Track Core Matrix:

The Y-axis is the "EDGE Momentum PR Score" (Momentum), representing the intensity of capital pursuit;

The X-axis is the "EDGE Fundamental PR Score" (Fundamental), representing the company's earnings quality.

The upper-right quadrant, 【Dual-Engine Resonance】, is our primary battlefield, representing capital momentum supported by fundamentals; the upper-left quadrant, 【Pure Speculation】, represents targets lacking fundamentals and relying purely on capital hype, requiring strict risk control.

Based on this framework, market capital flows this week focused on four main fronts: the 【AI Server and HPC Supply Chain】 led by Foreign Institutional Investors, 【Semiconductor Advanced Packaging and Domestic Equipment】 targeted by Domestic Fund Managers, the recovery of 【Networking, Consumer Electronics, and Optical Communications】 where capital began to return, and 【Niche Domestic Demand and Small/Mid-cap Turnaround Stocks】 for short-term plays by Speculative Capital. For the leaders and capital structure of each theme, please refer to the 【EDGE Dual-Track Core Matrix】 below.

EDGE Dual-Track Core Matrix

Tier 1|Macro Main Battlefield for Foreign Institutional Investors

- Battlefield Attribute: Tier 1 (Top 1-50 Liquidity)|Macro Main Battlefield for Foreign Institutional Investors

- Main themes this week: AI Server and HPC supply chain, networking, consumer electronics, and optical communication recovery. Foreign Institutional Investors are heavily betting on AI infrastructure-related supply chains, especially large CCL and substrate manufacturers with high technical barriers, where fundamentals and capital flows are resonating synchronously.

| EDGE Momentum PR Score | Ticker and Company Name | Core Capital Theme |

|---|---|---|

| 94.8 | 4958 Zhen Ding Tech | Apple supply chain PCB leader, strong recovery from Foreign Institutional Investors |

| 94.3 | 6223 MPI | Probe card leader, benefiting from explosive demand in AI chip testing |

| 91.3 | 6274 Iteq | 【Dual-Engine Resonance】 Strong demand for high-frequency high-speed CCL, aggressive buying by Foreign Institutional Investors |

| 91.2 | 3105 Win Semi | 【Dual-Engine Resonance】 PA demand warming up, benefiting from smartphone market recovery |

| 89.1 | 2313 Compeq | Dual themes of LEO satellites and server boards, favored by Foreign Institutional Investors |

| 88.9 | 2383 TUC | 【Dual-Engine Resonance】 Leading market share in AI server materials, solid earnings momentum |

| 88.1 | 2337 Macronix | 【Dual-Engine Resonance】 Improving memory market conditions, high fundamental score with defensive qualities |

| 87.7 | 3037 Unimicron | ABF substrate utilization rate rebounding, Foreign Institutional Investors continuing to position at low levels |

| 87.0 | 6285 WNC | Networking giant benefiting from US infrastructure, fundamentals yet to catch up |

| 85.4 | 3189 Kinsus | Substrate industry bottom has passed, Foreign Institutional Investors entry for positioning |

Tier 2|Mid-cap Growth Stocks for Domestic Fund Managers

- Battlefield Attribute: Tier 2 (Top 51-400 Liquidity)|Mid-cap Growth Stocks for Domestic Fund Managers

- Main themes this week: Semiconductor advanced packaging and domestic equipment. Equipment stocks led by Domestic Fund Managers showed a collective breakout, benefiting from CoWoS capacity expansion; multiple stocks have extremely high fundamental scores, providing long-term support.

| EDGE Momentum PR Score | Ticker and Company Name | Core Capital Theme |

|---|---|---|

| 99.8 | 3131 Grand Process Tech | 【Dual-Engine Resonance】 CoWoS wet process equipment leader, very high order visibility |

| 99.4 | 8096 Clientron | Samsung agent, benefiting from memory price hike themes |

| 99.3 | 6147 ChipMOS | Driver IC assembly and testing demand rebounding, Domestic Fund Managers actively positioning for catch-up |

| 98.9 | 6584 Nan Jun | Cloud service provider server rail demand driving earnings growth |

| 98.8 | 6451 Corning Tech | CPO optical transceiver module theme, Domestic Fund Managers focusing on transformation strength |

| 98.5 | 3583 Scientech | Dual growth engines in semiconductor wet process equipment and reclaimed wafers |

| 98.1 | 3026 HEC | Passive component inventory depletion ended, stock price strengthening from low levels |

| 98.0 | 3167 Ta Liang | PCB and semiconductor drilling machine demand recovering, strong stock price |

| 97.9 | 6727 AVC | 【Dual-Engine Resonance】 FPC and semiconductor coating equipment orders full, excellent fundamentals |

| 97.8 | 6640 Jun Hua | Sorters benefiting from advanced packaging capacity expansion, highly favored by Domestic Fund Managers |

Tier 3|Speculative Plays led by Speculative Capital

- Battlefield Attribute: Tier 3 (Top 401-1000 Liquidity)|Speculative Plays led by Speculative Capital

- Main themes this week: Niche domestic demand and small/mid-cap turnaround stocks. While large-cap stocks take a break, Speculative Capital seeks opportunities in small/mid-caps like biotech, gaming, and domestic demand; need to be mindful of fundamental gaps in trading.

| EDGE Momentum PR Score | Ticker and Company Name | Core Capital Theme |

|---|---|---|

| 99.7 | 4741 Hong Han | Inkjet ink niche market, extremely strong push by Speculative Capital |

| 99.5 | 6693 Anaprime | 【Dual-Engine Resonance】 PMIC and cooling drivers, excellent fundamental performance |

| 99.2 | 6547 Medigen | Vaccine theme resurfaces, but fundamentals remain in loss, caution required |

| 98.4 | 6024 Capital Futures | 【Dual-Engine Resonance】 Expansion of Taiwan stock trading volume, futures brokers' profits significantly improved |

| 98.3 | 3093 Kong Jian | Agent for semiconductor inspection equipment, extremely weak fundamentals, purely speculative |

| 98.2 | 3339 Tekcore | LED niche applications, strong momentum from oversold rebound |

| 97.7 | 6715 Jia Ji | High-speed cables benefiting from server spec upgrades, strong momentum |

| 97.0 | 2640 Taiwan Taxi | Domestic consumption driving taxi dispatch demand, steady profits |

| 96.3 | 3086 Wayi | Game update theme driven, weak fundamental support |

| 95.6 | 1210 Dachan | Feed and meat leader, defensive capital entering for catch-up |

Thematic Macro-Logic|AI Server and High-Performance Computing (HPC) Supply Chain

The arms race in AI servers and High-Performance Computing (HPC) has spread from Cloud Service Provider (CSP) capital expenditures to the strategic deployments of enterprises and sovereign nations, driving a multi-year infrastructure upgrade supercycle. The core characteristic of this demand cycle is the structural shift from "general-purpose computing" to "accelerated computing." The underlying logic is that the training and inference of Large Language Models (LLMs) and generative AI applications place exponential demands on computing power, power consumption, and transmission bandwidth. The traditional CPU-centric architecture can no longer meet these computing density requirements, and the focus of the battlefield has clearly shifted to accelerator clusters centered on GPUs and ASICs. This architectural transformation is fundamentally reshaping the value distribution of the server supply chain.

Iteration of technical specifications is the amplifier for this supply-demand structural reversal. The evolution from NVIDIA H100/H200 to the next-generation Blackwell GB200 platform is not just an improvement in single-chip performance but a comprehensive innovation in system-level design. Higher computing density means higher power consumption and heat flux density, while the leap in interconnect bandwidth (such as NVLink) poses unprecedentedly strict tests for the material properties of Printed Circuit Boards (PCB) and their substrate, Copper Clad Laminates (CCL). Signal transmission rates moving from 32 GT/s in PCIe Gen 5 to 64 GT/s in Gen 6 force CCL materials to upgrade from traditional Low Loss grades to Ultra Low Loss or even Extreme Low Loss grades to ensure signal integrity and reduce transmission loss. The reason Tier 1 Foreign Institutional Investors macro capital is willing to give extremely high valuation premiums to relevant material suppliers at this moment is precisely because they foresee this "re-rating" driven by technical upgrades. The market is no longer trading on simple shipment Volume, but on the structural and non-linear jumps in ASP and Gross Margin. Smart money expects upcoming financial reports to clearly verify that the rapid increase in the revenue share of AI-related products will translate directly into profitability exceeding past cycles and more stable long-term order visibility.

Core Leaders Micro-Insights

🎯 Core Leader Insight: 6274 Iteq

(1) Absolute Moat and Supply Chain Position

The core moat of 6274 Iteq is built on its deep R&D accumulation and customer certifications in the field of high-speed, low-loss materials. In the AI accelerator ecosystem, Iteq is not only a CCL supplier but also an enabler of key performance. Its products are widely used in the most core computing modules of AI servers, such as OAM (OCP Accelerator Module) motherboards and UBB (Universal Baseboard). These blocks are the lifeblood carrying GPUs and high-speed switches, placing extremely strict requirements on the material's dielectric constant (Dk) and dielectric loss (Df). With its leading layout in Extreme Low Loss grade materials, Iteq has secured its place in the reference design and certified supplier lists of major AI chip platforms such as NVIDIA, AMD, and Intel, forming a strong technical and certification barrier that effectively blocks competition from latecomers.

(2) Momentum Catalyst (Recent Marginal Changes)

The recent marginal change lies in the continuous upward revision of market expectations for the material specifications of the NVIDIA Blackwell platform. The system design of the GB200 far exceeds the H100/H200 generation in terms of requirements for signal integrity; not only do CCL layers significantly increase, but material grades must also be fully upgraded to higher-end products. This change means that the Content Value of Iteq in AI servers will see exponential growth. The momentum catalyst comes from positive signals continuously released by the supply chain: high-end material capacity remains tight, and order visibility has extended into the coming quarters. Its high EDGE Momentum PR Score of 91.3 reflects the rapid and intense re-pricing of market capital regarding its ASP and Product Mix optimization expectations.

(3) Dual-Track Fundamental Verification

The strategic label is clearly verified in the financial reports of 6274 Iteq. The first-track engine is the revenue scale expansion brought by the continuous growth of AI server shipments. The second-track engine is the structural improvement in profitability driven by the product mix shifting toward high-margin Ultra/Extreme Low Loss materials. Examining the quality of its financial reports, it can be observed that the rising share of AI-related application revenue has directly driven the company's overall gross margin out of the traditional server and networking product range into a new, higher platform. This profit growth model driven simultaneously by "volume" and "price" possesses high sustainability and defensiveness, which is the fundamental reason its EDGE Fundamental PR Score remains at a high of 90.8 and is why it is a long-term structural growth target sought by macro capital.

🎯 Core Leader Insight: 2383 TUC

(1) Absolute Moat and Supply Chain Position

The absolute moat of 2383 TUC is its near-monopoly market share and scale advantage in the global Halogen-Free CCL material market. Under ESG trends and AI server requirements for high power consumption and high reliability, halogen-free materials have become the mainstream specification. TUC, with years of technical leadership and capacity layout, has become the preferred or even exclusive supplier for major AI server ODMs and CSP brands in core components such as Switch Boards and accelerator modules. Its moat lies not only in technology but also in the stable delivery capability and quality consistency formed by its massive capacity, which has become an irreplaceable strategic value in the current race to build AI infrastructure.

(2) Momentum Catalyst (Recent Marginal Changes)

The momentum catalyst stems from the "winner-takes-all" effect in the AI supply chain. As AI server specifications become increasingly complex, customers tend to concentrate orders on leaders with the strongest technology and capacity for the sake of stability and performance. The marginal market change is that 2383 TUC's supply share in next-generation AI platforms has been confirmed to increase rather than decrease compared to the previous generation. This broke the concerns of some investors regarding intensified competition and reinforced its pricing power as an industry leader. Furthermore, the rapid rise in demand for AI ASIC chips (such as Google TPU, Amazon Trainium/Inferentia) has opened a second growth curve for TUC beyond GPUs, further expanding its Total Addressable Market (TAM) and providing strong support for stock price momentum.

(3) Dual-Track Fundamental Verification

The logic is reflected in the fundamentals of 2383 TUC through the dual blessing of market share expansion and product value enhancement. The first-track engine comes from the booming development of the overall AI server market. The second-track engine is its ability, based on its leading position, to not only obtain higher material ASPs in every specification upgrade but also capture a larger market share. The verification point of its financial report quality is that while revenue grows, the expansion rate of the operating margin is often faster than the revenue growth rate, which clearly reveals its strong operating leverage and superior cost control capabilities. The high EDGE Fundamental PR Score of 88.6 is an affirmation of its ability to maintain top-tier profitability in a high-growth track; such certainty is the core asset characteristic most favored by Tier 1 capital in volatile market environments.

Thematic Macro-Logic|Semiconductor Advanced Packaging and Domestic Equipment

The paradigm shift in the semiconductor industry is accelerating from Moore's Law scaling at the front end toward heterogeneous integration at the back end. This structural transformation is reshaping the value distribution of the global supply chain. Exponential growth in AI computing demand has propelled 2.5D/3D advanced packaging technologies like CoWoS from a niche market to a strategically contested capacity. Currently, the pricing power for capacity bottlenecks is fully held by the foundry leader. Its unprecedented capital expenditure expansion is overflowing orders and growth momentum into the local equipment and material supply chain through a clear transmission path. This is not just a cyclical recovery but a long-term structural re-rating catalyzed by technical specification upgrades and geopolitics (supply chain localization).

In this macro context, the capital flows of Tier 2 Domestic Fund Managers clearly reveal the market's expected path. The reason this core force is willing to give local equipment stocks an extremely high valuation premium at this moment is not based on current static P/E ratios, but on pricing the high-certainty growth of revenue and profit over the next 2 to 3 years. The market expects that as TSMC's CoWoS capacity expands rapidly from 15K WPM in 2023 to over 35K WPM by the end of 2025, the backlog of relevant supply chain manufacturers will translate into quarter-by-quarter revenue climbs over the coming quarters, accompanied by significant operating leverage release from economies of scale. Smart money is betting on this golden growth period from order visibility to actual financial realization. Their valuation system has shifted from traditional cyclical equipment stocks to platform-type growth stocks with long-term moats.

Core Leaders Micro-Insights

🎯 Core Leader Insight: 3131 Grand Process Tech

(1) Absolute Moat and Supply Chain Position

Grand Process Tech has established an unshakeable oligopolistic position in the field of semiconductor wet process equipment, especially in acid tank cleaning and single-wafer spin cleaning tools for advanced packaging, where it is a core supplier for TSMC's CoWoS expansion. Its moat comes not only from the long cycles and high thresholds of technical certification but is also deeply rooted in decades of co-development and process evolution with leading customers. In CoWoS production lines, wafer-level packaging yield is closely related to cleanliness. Grand Process Tech's equipment is a key node ensuring the yield of interposers and HBM stacking; its strategic position is far beyond that of a common equipment supplier, acting more as a "process enabler."

(2) Momentum Catalyst (Recent Marginal Changes)

Catalysts for market momentum come from the "accelerated schedule" and "upward revision of scale" for TSMC's CoWoS expansion. Original market estimates for expansion plans have continued to accelerate under the intense demand from AI chip giants, with the planning of the new Chiayi plant being the latest example. This marginal change has extended Grand Process Tech's order visibility from the original 6-8 months to 12-18 months, completely eliminating market concerns about its operational cyclicality. Capital is rapidly reacting to this expectation gap, viewing it as the highest-certainty "pick-and-shovel" play in the AI arms race within the Taiwan stock market.

(3) Dual-Track Fundamental Verification

The strategic label 【Dual-Engine Resonance】 is perfectly verified here. The first engine is the direct equipment orders brought by TSMC's CoWoS and SoIC expansion, which is the core driver for its revenue explosion and is already reflected in its surging contract liabilities and strong year-on-year revenue growth. The second engine is the high-margin consumables and maintenance service revenue that follows the massive shipment of machines. This "razor and blade" business model will provide stable and high-quality cash flow based on its massive installed base, further optimizing its profit structure and supporting its high EDGE Fundamental PR Score of 87.4.

🎯 Core Leader Insight: 6727 AVC

(1) Absolute Moat and Supply Chain Position

AVC targets another key bottleneck in the advanced packaging supply chain: ABF substrates and RDL (Redistribution Layer) processes. Its core products are high-end horizontal wet process equipment for immersion, coating, and lamination used in the PCB/IC substrate industry. When the constraints of CoWoS capacity spread from the wafer fab to the back-end ABF substrate supply, AVC's strategic value becomes prominent. Its moat lies in its deep understanding of substrate material characteristics and process physical limits, providing customers with one-stop solutions from material science to equipment integration. It is an indispensable partner for substrate leaders like Unimicron and Nan Ya PCB when expanding high-end capacity.

(2) Momentum Catalyst (Recent Marginal Changes)

The trigger for recent momentum is the market realizing that the specification requirements for ABF substrates in AI servers (larger area, more layers, finer line width) and the quantity demand have far exceeded existing capacity. This has triggered a new round of capital expenditure races among substrate manufacturers, with investment heavily concentrated on the high-end process equipment that AVC excels in. The marginal change in momentum is that the market narrative has shifted from "waiting for PC/NB inventory depletion" to "AI driving substrate industry specification upgrades and capacity expansion," leading to a fundamental reversal in AVC's order expectations.

(3) Dual-Track Fundamental Verification

The logic is reflected here as upstream-downstream transmission in the industrial chain. The first engine makes it an indirect beneficiary of TSMC's expansion effect. The explosion in CoWoS demand forces ABF substrate manufacturers to expand capacity simultaneously; AVC's equipment orders and revenue growth are direct manifestations of this trend. The second engine comes from domestic substitution through technical upgrades. In the past, such high-end equipment was mostly monopolized by Japanese and German manufacturers. AVC, with its technical strength and local service advantages, has successfully entered the core of the supply chain. Its high EDGE Fundamental PR Score of 98.4 reflects its enjoyment of higher market share and better profit margins under the domestic substitution trend, with high gross and operating margins being the best proof.

Thematic Macro-Logic | Recovery in Networking, Consumer Electronics, and Optical Communications

【Thematic Macro-Logic】

After more than a year of inventory correction, the supply-demand structure of global consumer electronics, networking, and optical communications is reaching a critical turning point. The underlying drivers stem from the convergence of three forces: first, terminal inventory levels have fallen to healthy states, and restocking demand is beginning to transmit from the channel side to the upstream, forming the initial signal of a positive cycle; second, the generational transition of technical specifications is brewing a new wave of replacements, with the commercialization of Wi-Fi 7, hardware spec upgrades for AI PCs and AI smartphones, and data center demand for 800G/1.6T optical modules collectively constituting clear catalysts for a product cycle upturn; finally, the easing of inflationary pressure at the macroeconomic level has allowed the purchasing power of end consumers and corporate capital expenditure intentions to gradually recover, providing a favorable macro environment for industry recovery.

At this temporal junction, the reason Tier 1 institutional capital (Foreign Institutional Investors and Domestic Fund Managers) is willing to grant higher-than-historical-average valuation premiums to relevant supply chains is not based on currently realized financial reports, but rather on pricing-in a forward-looking V-shaped earnings reversal over the next two to three quarters. The core expectation of this smart money is that as capacity utilization rates recover from the bottom, corporate operating margins will demonstrate astonishing operating leverage flexibility. The market is betting on a "dual turning point in gross margin and operating margin," expecting that a moderate recovery in revenue will be magnified by accelerated growth on the profit side, thereby driving earnings per share (EPS) to an unexpected growth slope. This is the core reason why capital is willing to position early and seize the advantage of a low base.

Core Leaders Micro-Insights

【Core Leaders Micro-Insights】

🎯 Core Leader Insight: 2337 Macronix

(1) Absolute Moat and Supply Chain Positioning

2337 Macronix, as a global leader in non-volatile memory (NVM), has built its moat on the dual technical barriers and market share advantages of Read-Only Memory (ROM) and NOR Flash. In the ROM market, it has long been an indispensable supplier for the gaming industry (such as Nintendo), possessing an oligopolistic position and stable cash flow contributions. In the NOR Flash field, the company has successfully penetrated the high-barrier automotive electronics and industrial control markets with high-quality, high-reliability products, moving away from the severe price volatility of consumer products and establishing solid customer relationships and pricing power. This diversified yet high-barrier product portfolio provides it with better defensiveness and earnings stability than its peers during global memory industry cycles.

(2) Momentum Catalysts (Recent Marginal Changes)

The most significant recent marginal change is that NOR Flash contract prices have shown signs of stabilizing after several quarters of decline, with some low-capacity products even seeing price hike signals, indicating that capacity control on the supply side has been effective while demand recovery is gradually manifesting. As restocking orders from consumer electronics customers (such as PC and IoT devices) begin to emerge, coupled with stable demand in the automotive and industrial sectors, the market expects Macronix's capacity utilization rate to climb from its trough. This dual bottom signal of "price stabilization and utilization recovery" is the key catalyst driving upward revisions in market valuation models.

(3) Dual-Track Fundamental Verification

Applying the "Catch-up Candidate" strategic label, the investment logic for 2337 Macronix is clear. Its stock price has been at a relatively low level over the past year, dragged down by consumer electronics inventory corrections. However, its high EDGE Fundamental PR Score of 93.4 reflects the company's ability to maintain a robust financial structure and operational efficiency even during a down cycle. The core of current capital positioning is the expectation that its gross margin will significantly improve as the utilization rate recovers. Once revenue returns to a growth track, its inherent high operating leverage will quickly translate into a profit rebound, leading to a qualitative change in financial report quality. The market is trading on the expectation gap between "surviving the bottom" and "recovery growth"; high fundamentals provide a margin of safety, while the industry turning point provides upside potential.

🎯 Core Leader Insight: 3105 Win Semi

(1) Absolute Moat and Supply Chain Positioning

3105 Win Semi is the absolute leader in global Gallium Arsenide (GaAs) wafer foundry, with a market share exceeding 70%, forming powerful economies of scale and technical moats. Its position in the Radio Frequency (RF) Power Amplifier (PA) field is unshakable, serving as a core supplier for major global smartphone brands (such as Apple and Samsung) and RF component design companies (such as Broadcom and Qorvo). The high technical barriers and expensive capital expenditures of GaAs processes effectively block new competitors, allowing Win Semi to play the key role of "arms dealer" in the supply chain for 5G smartphones, Wi-Fi infrastructure, and other critical applications, with the influence to define industry specs and trends.

(2) Momentum Catalysts (Recent Marginal Changes)

Marginal momentum catalysts mainly come from two aspects: first, global smartphone shipment volumes have confirmed a bottom reversal, with restocking strength in the Android camp being particularly significant, directly driving a rapid ramp-up in Win Semi's capacity utilization rate. Second, the commercial landing of the Wi-Fi 7 standard is initiating a new round of spec upgrade cycles. Compared to Wi-Fi 6, Wi-Fi 7 requires more complex and higher-end PA components, meaning the average selling price (ASP) and content value of Win Semi's products will increase significantly. The dual-engine recovery of smartphone and networking applications constitutes strong revenue growth momentum.

(3) Dual-Track Fundamental Verification

3105 Win Semi is a typical "Catch-up Candidate" target, as its profitability is highly correlated with capacity utilization. During the past industry down-cycle, low utilization rates put significant pressure on its financial performance, and its stock price remained low. However, a high EDGE Momentum PR Score of 91.2 indicates that market capital has keenly captured the trend of the utilization rate rebounding strongly from its trough (approx. 20% in Q1'23) and has entered the fray early. Institutional investors expect that as the utilization rate continues to climb past the break-even point, its profits will show exponential growth, demonstrating extremely high operating leverage benefits. The current market is not trading on its past losses but on the massive earnings elasticity brought by the recovery of utilization in future quarters. This is a precision strike on an operational turning point, with the smartphone market recovery and Wi-Fi 7 upgrade trend providing solid fundamental verification for this script.

Thematic Macro-Logic | Niche Domestic Demand and Small/Mid-Cap Turnaround Stocks

Currently, the Weighted Index is fluctuating in a high-level box pattern near historical highs, and the momentum of large-cap blue chips and core AI supply chains has paused, leading to a slowdown in institutional capital liquidity. This power vacuum creates an excellent tactical window for Tier 3 domestic capital and short-term Speculative Capital. The characteristic of this capital is high risk appetite, seeking extreme flexibility and high Beta effects; their goal is not long-term value investment, but rather finding small/mid-cap stocks that have not been fully priced by the market and possess strong narrative catalysts, intending to capture the sweet spot of a Davis Double Play (Valuation & EPS re-rating) within a 1-2 quarter timeframe.

The two main themes of "Niche Domestic Demand" and "Small/Mid-Cap Turnaround" perfectly align with the strategic needs of this smart money. The former, such as high-end niche financial services, can effectively isolate itself from global macro fluctuations and geopolitical risks, with its profit model directly benefiting from the heat and depth of the local capital market; the latter, such as electronic component manufacturers under specific spec upgrades, provides a script for profit and gross margin to rebound from the bottom. The market is willing to grant extremely high valuation premiums at this moment, betting not on currently realized financial figures, but on the expectation of non-linear growth in revenue and gross margins after specific catalysts ignite over the next 2-3 quarters. This is a gamble based on the "expectation gap," where smart money is positioning ahead of the stock price re-rating before financial figures are realized.

Core Leaders Micro-Insights

🎯 Core Leader Insight: 6693 Anaprime

(1) Absolute Moat and Supply Chain Positioning

Anaprime focuses on Brushless DC (BLDC) motor drive control IC design. Its core moat is built on analog and digital mixed-signal design capabilities, as well as a deep grasp of downstream end-application know-how. Compared to standard consumer ICs, BLDC drive ICs require customized tuning for different motor specs, cooling modules, and end products (such as server fans, high-end home appliances, power tools), creating high customer stickiness. Under the global trend of ESG and energy conservation, traditional brushed motors are rapidly being replaced by high-efficiency BLDC motors. Anaprime is at a key supply chain position in this structural transition, playing a core role in enabling end-product spec upgrades.

(2) Momentum Catalysts (Recent Marginal Changes)

The strongest recent momentum comes from the spec leap in AI server cooling demands. Traditional server fans have lower power consumption, but as GPU computing power surges to over 1000W, the complexity of cooling systems and the demand for fan speed and power consumption have grown exponentially. Anaprime has successfully entered the high-end server cooling fan supply chain, where the ASP and gross margins of its high-voltage, high-power BLDC drive IC products are much higher than those in consumer electronics applications, bringing a qualitative change to the company's revenue structure. This marginal change transforms it from a mature niche market participant into an indirect beneficiary of the AI computing power arms race.

(3) Dual-Track Fundamental Verification

Applying the Pure Speculation label, Anaprime's case is a classic example of "dreams meeting reality." Its high EDGE Fundamental PR Score of 94.1 already reflects significant improvements in year-on-year revenue growth and gross margins, verifying that the turnaround theme is not groundless. However, the core logic for the market granting it a high valuation is the bet that AI server cooling penetration will ramp up rapidly over the next few quarters, driving continuous optimization of its product mix. Current financial reports are just the beginning of the story; Speculative Capital is chasing the massive potential for a new business that currently accounts for single-digit revenue to grow into a major profit contributor of over 30%. The focus of financial quality observation will shift from revenue growth to the speed of increasing high-margin product ratios.

🎯 Core Leader Insight: 6024 Capital Futures

(1) Absolute Moat and Supply Chain Positioning

As one of the leaders in Taiwan's futures market, Capital Futures' moat comes from the oligopolistic nature of licensed financial businesses, a massive customer base and margin scale, and long-established brand reputation. In the capital market ecosystem, futures brokers play a core role in providing hedging and leverage trading tools, and their operational performance is highly positively correlated with overall market trading volume and volatility. Regardless of market direction, as long as price volatility and trading volume exist, their brokerage and proprietary trading businesses can generate stable profits—a classic "selling shovels" business model.

(2) Momentum Catalysts (Recent Marginal Changes)

The momentum catalyst does not come from within the company, but is a gift from the external macro environment. The Taiwan stock Weighted Index has repeatedly hit historical highs, trading volume continues to expand, and volatility remains at high levels, creating a golden age for futures and options trading. In particular, weekly expiring Taiwan Index Options (Weekly Options) have attracted a large number of short-term traders, with trading volumes repeatedly hitting new highs, directly boosting Capital Futures' brokerage commission income. This structural change has condensed Capital Futures' profit base from a monthly cycle in the past to a weekly cycle, simultaneously raising the stability and ceiling of its profits.

(3) Dual-Track Fundamental Verification

This ticker has less of a Pure Speculation component and is more of an ultimate manifestation of Niche Domestic Demand. Its high EDGE Fundamental PR Score of 95.8 directly and transparently reflects public data such as the average daily trading volume of Taiwan stocks and open interest in the futures market. The predictability of financial figures is extremely high, with almost no risk of an expectation gap. The market is granting it a valuation re-rating not in anticipation of an unknown turnaround, but in confirmation that the trend of "high trading volume as the new normal" will continue. In a market structure dominated by domestic capital and where day trading and short-term trading are prevalent, Capital Futures' profitability is seen as a Direct Beta Play on Taiwan stock capital momentum. As long as the market doesn't cool down rapidly, its steady profit growth trend possesses high certainty.

This week's capital battle needs no further explanation. This is a feast of spec upgrades driven by AI, mixed with a Speculative Capital party amidst high index levels. Capital is extremely concentrated in sectors with real order upgrades showing Dual-Engine Resonance, such as PCB, ABF, and advanced packaging. This is not a bull market where "all boats rise," but a winner-takes-all slaughterhouse. When chips in the main battlefield are highly locked in, any slight movement will trigger violent fluctuations; meanwhile, small/mid-cap turnaround stocks and catch-up themes in the peripheral battlefields are an ultimate test of human greed. The opportunity for momentum traders lies in the main tracks, while the risk comes from misjudging when the party will end.

The Absolute Iron Rules for Momentum Traders:

(1) Embrace the Premium: Valuation is an anchor for value investors, but a cage for momentum. The market is willing to pay a crazy premium for the fastest foreseeable growth; our task is to follow, not to question. For leaders in the Q1 quadrant, their only "fair price" is where the next higher-priced seller stands. Capital is dynamic; before the trend ends, any fear based on static valuation is simply handing Alpha returns to someone else.

(2) Ruthless Defense: The fuel of momentum is consensus, and "faith" is the anesthetic that leads to blown accounts. For those soaring stocks in the Q2 quadrant that are ignited purely by themes, they have no fundamentals to serve as a moat. The 5-day or 10-day moving average is your god. A break below is a betrayal, and exit discipline must be executed unconditionally, without excuse. Delete the words "averaging down" and "waiting for a rebound" from your dictionary.

Capital does not lie; discipline is the only tool that allows us to understand its language.

![[Semiconductor Consensus Tracking] 20260426 Trap Signals in the AI Frenzy](https://storage.ghost.io/c/45/e8/45e8af65-5e37-4e0a-95c0-7bd52e1935a5/content/images/size/w1200/2026/04/quadrant_20260426_en.png&q=100)