Interpretation of This Week's Capital Trends

This week, capital momentum is highly concentrated in AI-related infrastructure. The Tier 1 battlefield led by Foreign Institutional Investors (such as CCL/PCB and high-speed networking) is seeing concentrated chip holdings, with risks of chasing highs gradually increasing. Meanwhile, the index is fluctuating at high levels during the earnings gap period. Domestic capital and Speculative Capital have turned to ignite small-to-mid-cap, low-base turnaround themes. The market shows a phenomenon where the main battlefield is overheating while rotation in the guerrilla battlefields is accelerating. Operationally, more emphasis should be placed on momentum sustainability and risk discipline.

Our core logic is simple: do not guess bottoms or look for laggard rallies; only capture the leaders with the strongest price momentum in the entire market. To this end, the EDGE model divides the market into three battlefields based on liquidity: [Three Liquidity Tiers].

Tier 1 (Liquidity Top 1-50) is the macro main battlefield for Foreign Institutional Investors;

Tier 2 (Top 51-400) is the industrial hand-to-hand combat for Domestic Fund Managers;

Tier 3 (Top 401-1000) is the thematic speculation battlefield for Speculative Capital and domestic capital.

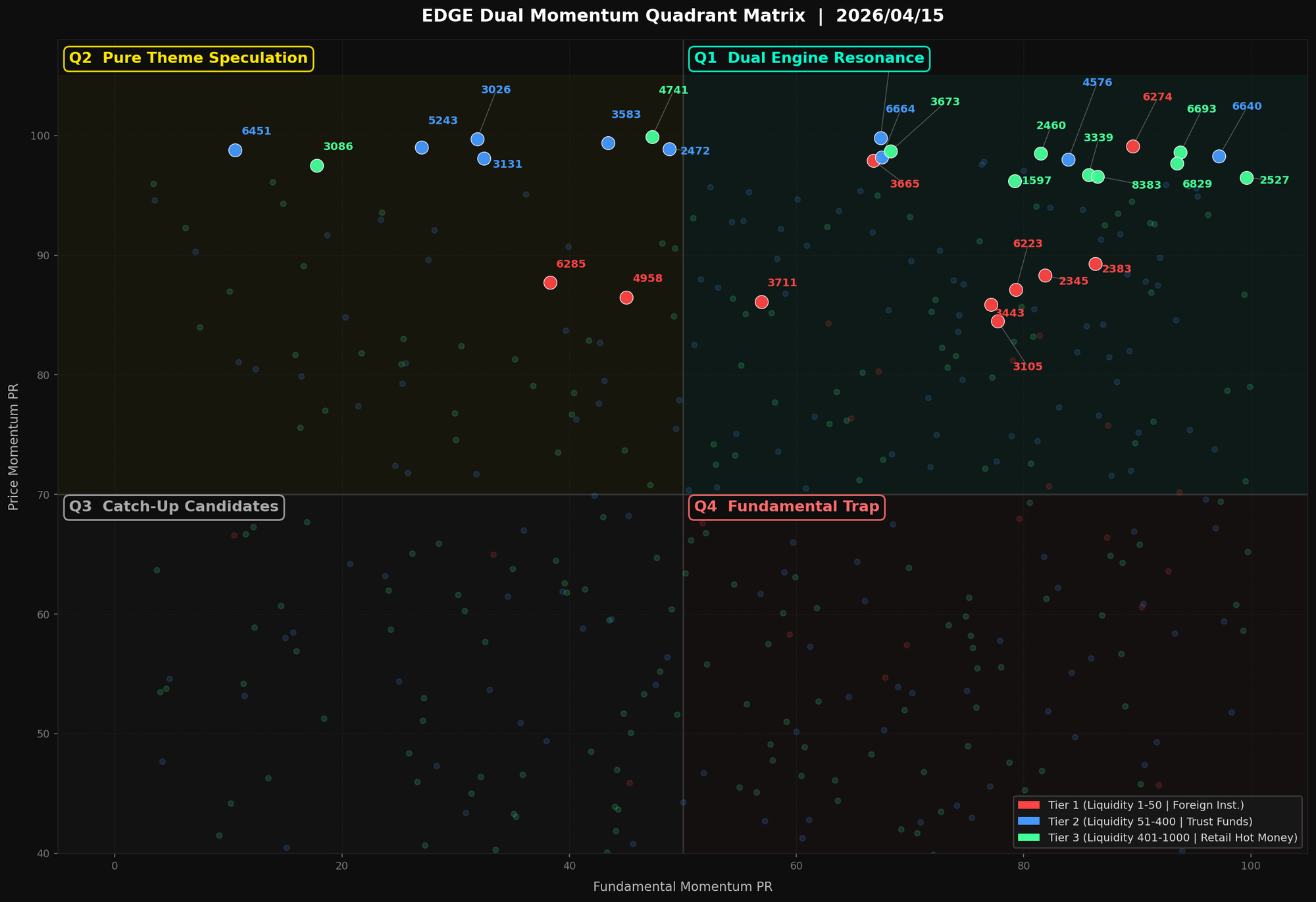

In each battlefield, we position stocks using a [Four-Quadrant Matrix]: with EDGE Fundamental PR Score as the X-axis and EDGE Momentum PR Score as the Y-axis. "Dual-Engine Resonance" stocks in the top-right quadrant represent the coexistence of fundamentals and capital momentum; "Pure Speculation" stocks in the top-left quadrant represent cases where fundamentals have yet to catch up, but capital momentum is extremely strong.

This week, the market's capital focus is clear, with four distinct battlefield boundaries: (1) Foreign Institutional Investors macro main battlefield: Dominated by [AI HPC and Networking Infrastructure], with high-end CCL and switches as the capital core. (2) Domestic Fund Managers performance battlefield: Targeting [Semiconductor Advanced Packaging and Inspection Equipment], chasing CoWoS expansion themes. (3) Speculative Capital ignition battlefield: Revolving around low-base themes such as [Precision Industry and Robotics] and [Electronic Component Recovery and Niche Applications] to find catch-up opportunities. For detailed stock positioning, please refer to the [Dual-Track Core Matrix] below.

EDGE Dual-Track Core Matrix

Tier 1|Foreign Institutional Investors Macro Main Battlefield

- Battlefield Attribute: Tier 1 (Liquidity Top 1-50) | Foreign Institutional Investors Macro Main Battlefield

- This Week's Main Themes: AI HPC and Networking Infrastructure. Foreign Institutional Investors concentrated their fire on AI infrastructure, especially CCL and high-speed switches with high technical barriers, supported by strong fundamentals.

| EDGE Momentum PR Score | Stock Ticker and Name | Core Capital Theme |

|---|---|---|

| 99.1 | 6274 Iteq | 【Dual-Engine Resonance】High-end CCL benefits from AI server volume growth; Foreign Institutional Investors strongly locking positions. |

| 97.9 | 3665 Bizlink | High-speed wiring harnesses penetrating AI chain; fundamentals recovering steadily. |

| 89.3 | 2383 TUC | 【Dual-Engine Resonance】AI server board leader; fundamentals and momentum hitting highs simultaneously. |

| 88.3 | 2345 Accton | Strong demand for 800G switches; a core long-term play for Foreign Institutional Investors. |

| 87.7 | 6285 WNC | Driven by the networking equipment replacement cycle; strong momentum but fundamentals need to catch up. |

| 87.1 | 6223 MPI | Probe cards benefiting from AI testing demand; high consensus between Foreign Institutional Investors and Domestic Fund Managers. |

| 86.5 | 4958 Zhen Ding Tech | PCB leader benefiting from both Apple and AI themes; momentum turning strong. |

| 86.1 | 3711 ASE Technology | OSAT leader benefiting from advanced packaging capacity overflow; Foreign Institutional Investors covering positions. |

| 85.9 | 3443 GUC | Long-term positive outlook for ASIC demand; momentum restarted after share price pullback. |

| 84.5 | 3105 Win Semi | Smartphone PA inventory depletion complete; Foreign Institutional Investors bullish on compound semiconductors. |

Tier 2|Domestic Fund Managers Core Growth Stocks

- Battlefield Attribute: Tier 2 (Liquidity Top 51-400) | Domestic Fund Managers Core Growth Stocks

- This Week's Main Themes: Semiconductor Advanced Packaging and Inspection Equipment. The semiconductor equipment and inspection group led by Domestic Fund Managers is benefiting from TSMC's advanced packaging expansion; some stocks have extremely strong momentum despite fundamentals not yet catching up.

| EDGE Momentum PR Score | Stock Ticker and Name | Core Capital Theme |

|---|---|---|

| 99.8 | 6830 ARES | Strong demand for semiconductor inspection and analysis; an active target for Domestic Fund Managers window dressing. |

| 99.7 | 3026 HEC | Passive component inventory depletion; purely a short-term capital safe haven. |

| 99.4 | 3583 Scientech | Wet process equipment entering CoWoS; thematic strength outweighs fundamentals. |

| 99.0 | 5243 E&R Engineering | Automotive and LEO satellite components; strong momentum but weak fundamentals. |

| 98.9 | 2472 Lelon | Aluminum capacitors benefiting from power electronics demand; fundamentals slowly rising. |

| 98.8 | 6451 Corning Tech | 【Pure Speculation】CPO Silicon Photonics theme gaining traction; capital chasing purely visionary themes. |

| 98.3 | 6640 Jun Hua | 【Dual-Engine Resonance】High visibility in packaging equipment orders; profit momentum is extremely strong. |

| 98.2 | 6664 Chiun Yu | PCB automation equipment benefiting from expansion; Domestic Fund Managers continuing to add positions. |

| 98.1 | 3131 Grand Process Tech | 【Pure Speculation】Advanced packaging equipment benchmark; overheated capital driving momentum to highs. |

| 98.0 | 4576 Hiwin Mikrosystem | 【Dual-Engine Resonance】Robotics and automation theme; fundamental performance exceeding expectations. |

Tier 3|Speculative Capital-Led Speculative Plays

- Battlefield Attribute: Tier 3 (Liquidity Top 401-1000) | Speculative Capital-Led Speculative Plays

- This Week's Main Themes: Precision Industry and Robotics Components, Electronic Component Recovery and Niche Applications. Speculative Capital is targeting precision industry stocks with robotics or aerospace themes; these stocks possess high momentum while fundamentals are turning around from the bottom.

| EDGE Momentum PR Score | Stock Ticker and Name | Core Capital Theme |

|---|---|---|

| 99.9 | 4741 Hong Han | Successful transformation in inkjet chemicals; Speculative Capital initiating extreme price movements. |

| 98.7 | 3673 TPK Holding | Touch module transformation toward automotive; low base attracting Speculative Capital entry. |

| 98.6 | 6693 Anaprime | Power semiconductor R&D yielding results; fundamentals showing explosive potential. |

| 98.5 | 2460 Kian Tong | Rising copper prices driving terminal product quotes; fundamentals showing significant improvement. |

| 97.7 | 6829 Chien Fu Precision | 【Dual-Engine Resonance】Aerospace and semiconductor equipment dual-track progress; targeted by Speculative Capital. |

| 97.5 | 3086 Wayi | Game update themes; extremely weak fundamentals, purely capital speculation. |

| 96.7 | 3339 Tekcore | LED transformation to specialty lighting; fundamental improvement attracting Speculative Capital. |

| 96.6 | 8383 Chien Fu | Steady demand for plant engineering and precision parts; strong momentum for laggard rally. |

| 96.5 | 2527 Hong Jing | 【Dual-Engine Resonance】Peak period for construction project completion bookings; a laggard stock with extremely strong fundamentals. |

| 96.2 | 1597 TBI Motion | Recovery in linear slide rail demand; a benchmark for laggard rallies in industrial automation. |

Thematic Macro-Logic|AI High-Performance Computing and Networking Infrastructure

Capital flows in the macro battlefield are clearly pointing to a structural inflection point: AI computing power deployment has evolved from conceptual speculation into an arms race for technological hegemony. Its demand for underlying hardware infrastructure is triggering a profound shift in supply-demand structures. The cyclical inventory adjustments previously dominated by consumer electronics are no longer the primary contradiction; they have been replaced by a capital expenditure frenzy from Cloud Service Providers (Hyperscalers) and enterprises deploying Large Language Models (LLM). The key characteristics of this demand cycle are its "asymmetry" and "high-specification lock-in"—meaning demand is not only growing exponentially in quantity but also undergoing a generational leap in technical specifications, directly locking in the highest-end computing and transmission materials.

The core of this computing-driven paradigm shift lies in breaking data transmission rate bottlenecks. From the transition of Ethernet switches from 400G to 800G/1.6T, to the upgrade of internal server buses from PCIe Gen 4 to Gen 5/Gen 6, every doubling of bandwidth imposes stricter signal loss (Dk/Df) requirements on Copper Clad Laminates (CCL), the base material for Printed Circuit Boards (PCB). Traditional materials are no longer sufficient, and market demand is highly concentrated among a few oligopolistic suppliers capable of mass-producing Ultra Low Loss (ULL) or even Extreme Low Loss (ELL) grade CCL. Tier 1 Foreign Institutional Investors are currently willing to grant high valuation premiums to such targets precisely because they clearly foresee a multi-year "growth in both volume and price" supercycle brought about by this spec upgrade. Smart money is trading on the structural optimization of gross margins driven by the sharp increase in high-end product mix over the next 2-4 quarters, as well as the robust growth momentum resulting from highly certain terminal demand.

Core Leaders Micro-Insights

🎯 Core Leader Insight: 6274 Iteq

(1) Absolute Moat and Supply Chain Position

The moat of Iteq (6274) is built upon deep accumulation in materials science and long-term certification barriers with top-tier customers. As a leading global supplier of high-frequency and high-speed CCL, it shares an oligopoly in the Extreme Low Loss (ELL) material field with American and Japanese peers. The company is not only a major material supplier for the reference designs of AI chip giants like NVIDIA and AMD but also deeply penetrates the supply chains of new-generation server platforms from Intel and AMD (such as Eagle Stream and Genoa/Turin). This model of co-development and synchronized certification makes its market share in critical applications like AI servers and high-end switches difficult to shake, forming strong supply chain stickiness and pricing power.

(2) Momentum Catalysts (Recent Marginal Changes)

The core catalyst for recent momentum comes from the significant acceleration in 800G switch shipments and strong market expectations for the ramp-up of the NVIDIA Blackwell platform. These applications mandatorily require M7/M8 grade ELL materials, and Iteq (6274) is a core supplier for these specs. The marginal change lies in the fact that while the market previously worried about the penetration rate of high-end materials, data center customers have now made them standard equipment to ensure AI cluster computing performance. This shift means Iteq (6274)'s high-margin product lines are moving from niche markets to mainstream applications, with shipment momentum and product mix optimization trajectories far exceeding previous market expectations.

(3) Dual-Track Fundamental Verification

Applying the [Dual-Engine Resonance] strategy label, the fundamentals of Iteq (6274) exhibit typical dual-track driving characteristics. The first track is the "AI Computing Engine," dominated by GPU servers and AI accelerators, contributing the demand volume and revenue cornerstone for highest-spec materials. The second track is the "High-Speed Transmission Engine"; as 800G switches and PCIe Gen 5 servers become ubiquitous, its high-end materials further diffuse into the broader networking and server markets. Regarding financial quality, focus should remain on whether gross margins can break through the upper bound of historical ranges and whether the revenue share of high-end networking and server applications continues to climb. An EDGE Momentum PR Score of 99.1 resonating with an EDGE Fundamental PR Score of 89.6 reflects that market capital has fully recognized its profitability is entering a structural leapfrog channel.

🎯 Core Leader Insight: 2383 TUC

(1) Absolute Moat and Supply Chain Position

TUC (2383) has long cultivated halogen-free eco-friendly substrates and successfully extended this technical advantage into the high-frequency and high-speed fields, constructing a differentiated competitive barrier. Its critical position in the AI server supply chain is evidenced by its role as a core material supplier for OCP Accelerator Modules (OAM) and UB/UBB (Universal Baseboard), directly positioning itself at the heart of AI computing units. The company maintains close relationships with American cloud service giants and server ODM manufacturers, ensuring a high market share in next-generation AI hardware architectures through customized development and forward-looking capacity deployment. Its moat is a synthesis of technical patents, environmental trends, and deep terminal customer binding.

(2) Momentum Catalysts (Recent Marginal Changes)

The marginal catalyst for momentum stems from the continuous upward revision of AI server shipment estimates and the confirmation of TUC (2383)'s supply share therein. As major cloud customers announce their staggering capital expenditure plans, visibility for demand in high-unit-price, high-spec substrates like OAM/UBB has significantly increased. Recent channel checks within institutional circles show that the company's share in major AI projects is solid or even increasing, dispelling previous market concerns regarding potential competitors. This increase in certainty is a key factor driving its stock momentum (EDGE Momentum PR Score 89.3) to catch up with industry leaders.

(3) Dual-Track Fundamental Verification

The logic is equally clear for TUC (2383). Its "AI Computing Engine" is primarily driven by large AI server orders from American CSP customers, serving as its strongest driver for revenue and profit growth. Meanwhile, its "Transmission Equipment Engine" is reflected in high-speed material demand brought by upgrades in high-end switches, routers, and general-purpose servers. Notably, besides AI servers, the spec upgrade of basic networking equipment is a massive and stable market, providing a second layer of growth protection for the company. The focus for verifying financial quality lies in whether AI-related revenue share can meet company guidance and the extent of operating margin expansion accompanying increased capacity utilization and product mix optimization. Its EDGE Momentum PR Score and EDGE Fundamental PR Score (86.3) are simultaneously at highs, indicating the market is actively pricing in its core beneficiary status in the AI infrastructure expansion wave.

Thematic Macro-Logic|Semiconductor Advanced Packaging and Inspection Equipment

【Thematic Macro-Logic】

The computing power arms race sparked by Generative AI is rapidly shifting the semiconductor industry's value chain bottleneck from front-end wafer fabrication to back-end advanced packaging. High-end AI chips from NVIDIA, AMD, and others generally adopt Chiplet designs, making reliance on 2.5D/3D packaging technologies like CoWoS (Chip-on-Wafer-on-Substrate) a source of non-linear growth. The core contradiction in the current market is that terminal AI demand is exploding exponentially, while the CoWoS capacity supply from the leading foundry is expanding linearly, creating a severe supply-demand imbalance. This structural gap has forced major players like TSMC to initiate the largest advanced packaging capital expenditure in history, directly triggering an order visibility and valuation re-rating cycle for the upstream equipment supply chain.

The "Smart Money" at this stage, particularly Tier 2 Domestic Fund Managers pursuing high growth elasticity, is trading not on current financial reports but on "order conversion rates" and "gross margin structural optimization" expected to occur within the next 12-18 months. The market is willing to grant high valuation premiums, betting on the certainty of CoWoS expansion plans translating from press releases into actual equipment Purchase Orders (PO). These funds expect the revenue and profit of relevant equipment manufacturers to show leapfrog growth in the next 2-4 quarters, far exceeding existing market expectations. The current strength in stock price momentum is a "front-running of expectations before earnings realization," reflecting a consensus convergence on the biggest beneficiaries of the capacity expansion cycle.

Core Leaders Micro-Insights

【Core Leaders Micro-Insights】

🎯 Core Leader Insight: 6640 Jun Hua

(1) Absolute Moat and Supply Chain Position

Jun Hua (6640) plays the critical role of the "Eye of Precision Machinery" in the advanced packaging field. Its core moat lies in high-precision Pick & Place and Die Bonding technologies. In the CoWoS process, extremely tiny Logic Dies and HBM (High Bandwidth Memory) must be precisely attached to the Silicon Interposer, requiring micron-level accuracy. Jun Hua possesses deep technical accumulation and a track record of customer certification in this field. As a core equipment provider in TSMC's CoWoS supply chain, its position is difficult to replace. Its products directly correspond to the most critical bottleneck processes in CoWoS capacity expansion, making it a pure beneficiary of this expansion round.

(2) Momentum Catalysts (Recent Marginal Changes)

The core catalyst for momentum comes from the continuous upward revision of TSMC's CoWoS capacity targets. From the initial 15,000 wafers per month to recent market rumors of challenging 35,000 by year-end, and even doubling the target for 2025, every upward adjustment of capacity targets directly corresponds to an expansion of Jun Hua's potential order scale. Its EDGE Momentum PR Score stands at a high 98.3, reflecting the market's extreme optimism in discounting these long-term capacity targets into current stock price momentum. The marginal change is that the market now views Jun Hua as an "Alpha" indicator for CoWoS capacity expansion, with its stock performance highly correlated to the capital expenditure plans of packaging and testing leaders.

(3) Dual-Track Fundamental Verification

Applying the [Pure Speculation] label, Jun Hua (6640) belongs to the category of "having both dreams and reality." Its high EDGE Fundamental PR Score of 97.2 indicates the company already possessed excellent profitability and operational health before the theme exploded. This means that massive CoWoS orders are not merely rescuing a poorly performing company but are providing an epic growth opportunity for an already high-performing enterprise. The market's dual-track verification logic is: existing robust fundamentals provide downside protection for valuation, while the explosive orders from CoWoS open the ceiling for valuation upside. High fundamental scores allow Domestic Fund Managers to chase the dream while still finding a solid financial basis for support.

🎯 Core Leader Insight: 3131 Grand Process Tech

(1) Absolute Moat and Supply Chain Position

The moat of Grand Process Tech (3131) is established on its status as a "Wet Process Chemical Expert" in the packaging process. Its core business includes single wafer spin scrubbers, photoresist strippers, and etchers. In the complex structure of CoWoS, whether it is Deep Silicon Etching (DSE) of the interposer or the development, etching, and cleaning of the RDL (Redistribution Layer), high-performance wet process equipment is indispensable. Leveraging years of experience in co-development with wafer foundries, Grand Process Tech has built high customer stickiness in specific chemical formulas and machine integration, forming an unshakable supply chain positioning advantage.

(2) Momentum Catalysts (Recent Marginal Changes)

Similar to Jun Hua, its momentum catalyst is also the frantic expansion of CoWoS. However, the market's perception of marginal changes for Grand Process Tech is even more intense. Previously, the market classified it as a more traditional packaging equipment provider, but recently, institutional capital has begun to rediscover its high value-add and indispensability in the CoWoS process chain. An EDGE Momentum PR Score of 98.1 indicates the market is undergoing a "value rediscovery," with capital inflows based on expectations that its share of CoWoS orders will see a structural and permanent increase.

(3) Dual-Track Fundamental Verification

Grand Process Tech (3131) is a perfect embodiment of the [Pure Speculation] label. Its EDGE Fundamental PR Score of only 32.5 points directly to its relatively mediocre past financial performance, which had not entered a high-growth trajectory. However, under the current trading framework, this has become the strongest narrative foundation. The market completely ignores historical financial reports, viewing it as a "clean canvas" ready to receive a brand-new profit blueprint brought by CoWoS. A low fundamental base means the slope of financial improvement driven by new orders will be extremely steep, with massive potential for earnings surprises. Momentum traders are betting on this dramatic "mediocre to excellence" transition; the stock momentum leads fundamentals by several quarters, serving as advance pricing for a total transformation in future profitability.

Thematic Macro-Logic | Precision Industry and Robot Components

Global manufacturing PMI data has moderately recovered from its cyclical bottom, and the inventory destocking cycle is nearing its end, signaling that a new capital expenditure cycle is brewing. Against this macro backdrop, market liquidity has begun to permeate from overcrowded high-level themes like AI servers and thermal management into industrial recovery sectors with laggard recovery potential. Precision industry and robot components, as leading indicators of global end-manufacturing sentiment, are at a critical tipping point where order visibility is rebounding from the bottom. These targets have had a low financial reporting base over the past year; once revenue momentum is confirmed to be warming up, operating leverage will bring extremely high profit elasticity.

Currently, the Tier 3 Speculative Capital and domestic institutional investors dominating this battlefield are not trading based on realized financial figures, but are proactively pricing in the order recovery and gross margin expansion expected over the next 2-3 quarters. This "smart money" is willing to grant higher valuation premiums at this moment, with the core focus being on capturing the "slope of change" as revenue and profit transition from negative to positive growth, rather than absolute levels. The market expects that as demand for end-applications such as semiconductor equipment, automated production lines, and aerospace gradually rolls out, the relevant supply chain will encounter substantive earnings delivery, thereby validating the current strong stock price momentum. The appeal of this theme lies in its clear industrial logic, relatively clean shareholding structure, and a lower expectation baseline compared to mainstream electronic stocks, providing asymmetric risk-reward opportunities.

Core Leaders Micro-Insights

🎯 Core Leader Insight: 6829 Chien Fu Precision

(1) Absolute Moat and Supply Chain Status

Chien Fu Precision has established deep barriers in the field of high-end precision machining. Its core moat comes from certifications and customer relationships in two high-entry-barrier markets: aerospace and semiconductor equipment. In the semiconductor field, the company is a core supplier of vacuum chambers and key components for the world's largest semiconductor equipment manufacturer. Its process capabilities and quality stability have been long-verified, making its position difficult to replace. In the aerospace field, its products such as engine casings have passed certifications from major international manufacturers, belonging to an oligopolistic market with long-term contract orders that provide a stable cash flow base. This dual-engine structure makes it more defensive during fluctuations in any single industry.

(2) Momentum Catalyst (Recent Marginal Changes)

Marginal momentum primarily comes from two aspects: First, global semiconductor giants have restarted a new round of capital expenditure, especially the demand for expansion in advanced processes, which directly drives the procurement of upstream equipment components. Second, global air traffic has strongly recovered post-pandemic, driving a massive backlog for aircraft manufacturers like Boeing and Airbus into an accelerated delivery phase, resulting in structural growth in demand for key engine components. This dual tailwind overlap constitutes a strong revenue growth catalyst.

(3) Dual-Track Fundamental Verification

Applying the [Laggard Recovery] strategic label, the aerospace and semiconductor equipment businesses of Chien Fu Precision have lagged behind mainstream tech stocks over the past year due to inventory adjustments by end customers. Its high EDGE Fundamental PR Score of 93.5 reflects the company's ability to maintain excellent profitability and financial structure even during industrial headwinds. Now that the industry sentiment has reached a turning point, its high-quality fundamental base will allow it to demonstrate the strongest Operating Leverage when revenue rebounds. The market is precisely trading on this expectation of shifting from "defensive high-quality" to "aggressive high-growth."

🎯 Core Leader Insight: 4576 Hiwin Mikrosystem

(1) Absolute Moat and Supply Chain Status

As a core enterprise under the Hiwin Group specializing in precision motion and control components, Hiwin Mikrosystem's moat is built on the technical depth of "mechatronic integration" and group synergies. Its main products, such as linear motors, torque motors, and drivers, are the core factors determining the precision of "mother machines" like machine tools, semiconductor equipment, and automated production lines. Compared to simple mechanical processing, Hiwin Mikrosystem integrates motors, drives, and control algorithms to provide high-value-added solutions. Backed by the Hiwin Group's global channels and brand power, it possesses significant advantages in customer acquisition and supply chain management.

(2) Momentum Catalyst (Recent Marginal Changes)

The catalyst comes from the wave of automation upgrades triggered by the manufacturing industry's pursuit of resilience and efficiency under the trend of global supply chain restructuring. Whether in electronics assembly, automotive manufacturing, or logistics warehousing, investment demand for smart factories is recovering from the bottom. Signals from recent machine tool industry exhibitions and order data in the Asian region both indicate that the willingness for manufacturing capital expenditure is warming up. Hiwin Mikrosystem, as a "heart" supplier for automation equipment, sees its order status as a leading indicator for overall industrial sentiment, and this indicator has shown signs of bottoming out and rebounding.

(3) Dual-Track Fundamental Verification

Hiwin Mikrosystem is a typical representative of automation within the [Automation and Aerospace Components Benefit from Industrial Recovery] theme. Its operations are highly correlated with the machine tool and overall manufacturing sentiment; it previously bore the full pressure of the cyclical downturn, resulting in an extremely low revenue and profit base. Recently, monthly and annual revenue growth rates have begun to show a turning point from negative to positive. This "pivot" is precisely the signal momentum traders focus on most. Although the EDGE Fundamental PR Score (83.9) is not as high as Chien Fu Precision, this also reflects its higher sensitivity to the economic cycle (High Beta). Once the recovery trend is established, the slope of its profit improvement will be extremely steep. The EDGE Momentum PR Score of 98.0 is a premature market reaction to this drastic pivot expectation.

Thematic Macro-Logic | Electronic Component Recovery and Niche Applications

The electronic component inventory correction cycle has reached its end. While end-applications like PCs and smartphones show only moderate recovery, the driving force of the supply chain has quietly shifted. AI computing demand has spread from cloud GPUs to the edge, placing requirements for specification leaps in areas such as high-speed transmission, advanced packaging, thermal management, and power management. This structural shift has created niche growth tracks independent of the general economic cycle, becoming the core focus for current market capital. In this round of market action led by Tier 3 Speculative Capital, the market has shown a high preference for "transformation narratives," willing to pay extremely high valuation premiums for companies with the potential to break into new applications and escape old cut-throat battlefields.

The core logic of this smart money is not based on current financial reports, but on the expectation of a qualitative change in revenue structure and gross margin mix over the next 2-4 quarters. They are betting that companies can successfully pivot from low-margin mature markets (such as consumer electronics) to high-margin niche markets (such as AI data centers and CPO packaging). Therefore, at this stage, financial figures—especially profitability—often show a huge divergence from stock price momentum. The market is trading the convergence of the "expectation gap" rather than the rationality of the "P/E ratio." The earnings realization path capital expects to see is a significant ramp-up in the revenue share of new businesses; even if it might erode overall profits initially, as long as the revenue trend is established, momentum can continue.

Core Leaders Micro-Insights

🎯 Core Leader Insight: 2527 Hong Jing

(1) Absolute Moat and Supply Chain Status

The traditional moat of 2527 Hong Jing comes from its track record in construction and development, particularly its close link with the ASE Technology group, giving it a unique advantage in industrial plant and tech park development. Its supply chain status is not that of a traditional electronic component manufacturer, but rather an "infrastructure enabler" at the uppermost stream of the semiconductor industry chain. Amid the wave of global AI chip giants aggressively expanding advanced packaging (such as CoWoS) capacity, Hong Jing's role has transformed from a traditional property developer to a key partner for cleanrooms and plant construction that meet high specifications and short delivery requirements.

(2) Momentum Catalyst (Recent Marginal Changes)

The core catalyst for momentum stems from the market's "Re-rating" of its business structure. The market no longer views it as a cyclical construction stock, but as an infrastructure concept stock highly linked to the AI capital expenditure cycle. The recent marginal change lies in the market's expectation that it will undertake more urgent expansion orders from semiconductor customers responding to AI demand. The technical threshold and gross margin levels for such plant construction are far higher than traditional residential or commercial buildings. Momentum reflects the strong expectation of its order visibility and profit structure optimization over the coming years.

(3) Dual-Track Fundamental Verification

This target exhibits a special pattern of a [Fundamental Trap]. Its high EDGE Fundamental PR Score of 99.6 reflects steady profits from past real estate development recognitions; this is "existing fundamentals." However, its strong EDGE Momentum PR Score of 96.5 is built entirely on "incremental fundamentals" not yet fully apparent in financial reports—namely, AI-related plant construction projects. The key to verification lies in observing whether the proportion of high-margin tech plants in its order book or new contracts continues to rise as expected. If the contribution of new business cannot keep up with the high expectations implied by the stock price, existing steady profits will not be enough to support a valuation that has already broken away from traditional P/E ratio frameworks.

🎯 Core Leader Insight: 6451 Corning Tech

(1) Absolute Moat and Supply Chain Status

Affiliated with the Hon Hai Group, the core moat of 6451 Corning Tech lies in its years of deep cultivation in System-in-Package (SiP) technology. In the supply chain, it plays the role of a professional Outsourced Semiconductor Assembly and Test (OSAT) provider. As AI data center internal transmission rate requirements grow exponentially, traditional pluggable optical components hit bottlenecks, and Co-Packaged Optics (CPO) has become the industry-recognized solution. Corning Tech, leveraging its SiP technology foundation, has entered the CPO and optical communication module packaging fields, elevating its supply chain status from a consumer electronics accessory provider to a potential key supplier for core AI hardware network architectures.

(2) Momentum Catalyst (Recent Marginal Changes)

The ignition point for momentum is the market's confirmation that its CPO technology has entered the sample verification stage for North American Cloud Service Provider (CSP) customers. This marginal change represents the company moving from the "concept" stage to the eve of "commercialization," triggering a narrative-driven stock price reaction. The market is trading on the expectation that once it passes verification, it will enter a multi-year high-growth cycle. Any news regarding CPO technical progress, successful customer verification, or accelerated industry adoption becomes fuel to strengthen its momentum.

(3) Dual-Track Fundamental Verification

This is a typical [Fundamental Trap] case. Its EDGE Momentum PR Score is as high as 98.8, while its EDGE Fundamental PR Score is only 10.6, showing that its stock price performance is completely decoupled from its current profitability. Its existing financial reports reflect the weakness of its legacy consumer electronics SiP business, which is exactly where the "trap" of the stock price lies—any analysis based solely on historical financials would lead to an extremely negative conclusion. The focus of dual-track verification must be entirely on the progress of the new business: When will CPO-related products start contributing to revenue? What will the initial gross margin levels be? Can it successfully transition from NRE (Non-Recurring Engineering) income to mass production revenue? If the revenue contribution from the new business fails to materialize, or if gross margins after mass production are lower than expected, the "castle in the air" built by strong momentum will face severe correction risks.

This week's capital flow is not a comprehensive bull party, but a highly concentrated feast of specification upgrades. The main battlefield is clear: Tier 1 supply chains driven by AI computing demand, from high-end PCB/CCL to switches, where capital unhesitatingly pays for certainty premiums—this is the hunting time for institutional funds. However, overflowing Speculative Capital is causing a stir in peripheral battlefields; Pure Speculation in advanced packaging and laggard recoveries in industrial automation have become short-term parties, creating extremely high volatility. This means that the current game is half faith and half illusion. In the main battlefield, your opponent is the trend itself; in the periphery, your opponent is human greed. Opportunities and traps are separated by a thin line, and exposure management determines the final outcome.

(1) Embrace the Premium: Remember, "the strong stay strong" is the core of momentum. Don't waste time questioning the P/E ratios of leaders in the Q1 quadrant, and certainly don't fear because they "have already risen too much." Valuations are static reports from accountants, while capital flows are real-time intelligence from the battlefield. Our task is not to find value troughs, but to ride the strongest waves of capital. For true trend leaders, every pullback is a filtering of noise, not a trend reversal.

(2) Ruthless Defense: The only fatal flaw in momentum trading is turning a trade into a faith. For Pure Speculation stocks in the Q2 quadrant driven by stories, dreams, and valuation repairs, their lives depend entirely on market sentiment. Sentiment comes fast and leaves faster. The 5-day line is the attacking line, and the 10-day line is the lifeline. Once broken, there is no room for illusion, analysis, or waiting for a rebound. Discipline means immediate execution of stop-losses and unconditional exit. Leave your emotions for your family and bring discipline back to the trading room.

The market doesn't care about your opinions; it only responds to the most ruthless capital pressure.

![[Semiconductor Consensus Tracking] 20260426 Trap Signals in the AI Frenzy](https://storage.ghost.io/c/45/e8/45e8af65-5e37-4e0a-95c0-7bd52e1935a5/content/images/size/w1200/2026/04/quadrant_20260426_en.png&q=100)